What a leveraged buyout is, how it works and why PE firms use this high-stakes strategy to acquire companies and maximize returns.

What a leveraged buyout is, how it works and why PE firms use this high-stakes strategy to acquire companies and maximize returns.

Leveraged buyouts represent one of the most sophisticated and possibly the most controversial strategies in corporate finance.

At the same time, these transactions have created billionaire investors, transformed entire industries, and occasionally left companies struggling under crushing debt loads.

If you've ever wondered how a small group of investors can acquire billion-dollar companies without having billions in cash, you're looking at the magic—and the risk—of financial leverage.

The reality is both simpler and more complex than most people realize.

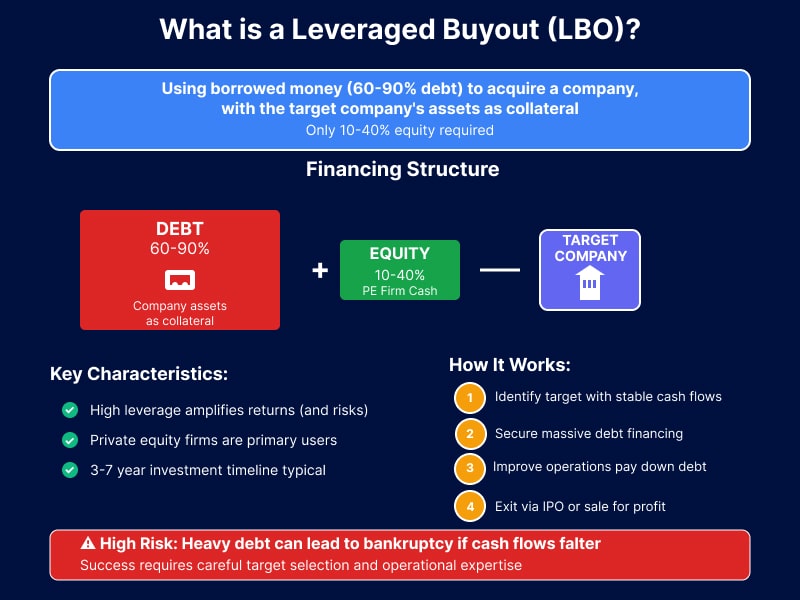

A leveraged buyout (LBO) is a financial transaction where investors acquire a company using a significant amount of borrowed money—typically 60% to 90% of the purchase price—with the acquired company's assets serving as collateral for the loans.

The remaining 10% to 40% comes from the buyer's equity investment.

At its core, a leveraged buyout uses the target company's own assets and future cash flows as collateral for the debt used to buy it.

Think of it as using a house's value to secure the mortgage that purchases it, except the stakes are measured in hundreds of millions or billions of dollars.

This financing structure creates powerful leverage effects that can amplify returns dramatically.

When successful, LBOs generate outsized profits for investors through a combination of debt paydown, operational improvements, and multiple expansion. When unsuccessful, the heavy debt burden can push companies toward bankruptcy.

LBOs are very different from traditional acquisitions in their financing approach.

Where a standard corporate acquisition would primarily use cash or stocks, an LBO deliberately maximizes debt to minimize the equity required for purchase.

The reason?

To amplify possible returns.

A leverage-heavy approach like an LBO, however, requires careful target selection and the most sophisticated of financial engineering.

Private equity firms dominate the LBO landscape, though strategic buyers and management teams occasionally structure leveraged transactions.

The LBO model aligns particularly well with private equity's investment thesis:

Acquire undervalued companies, improve operations, and exit at higher valuations within 3-7 years.

The LBO process follows a structured sequence designed to maximize returns while managing the inherent risks of high leverage:

The entire LBO process follows a logically sequenced structure aimed at maximizing returns while managing the embedded risks of high

Private equity firms sift through thousands of potential targets in search of those with predictable cash flows, market-leading positions, and opportunities to improve operations. Standard initial valuations include EBITDA multiples and discounted cash flow models as a means to establish baseline pricing.

The buyer sets up a capital structure ranging from 60-90% debt, which involves various tranches. This structure includes senior secured debt, subordinated debt/mezzanine debt, and equity, which represents the remaining portion ranging from 10-40%.

Financial, operational, and legal due diligence confirms the investment hypothesis while also pointing out potential opportunities for value creation. Deal structure negotiations include issues related to corporate governance, management incentives, and exit strategies.

Having raised the financial commitment necessary, along with having obtained the regulatory approvals, the deal can close. The existing debt in the target company, along with the equity, will normally change hands because the LBO debt has transferred.

After the acquisition, the attention shifts to implementing the investment thesis based upon cost cuts, growing the business through revenue initiatives, acquisitions, as well as process improvements. The management teams are usually offered extensive equity incentives.

After 3-7 years, the private equity firm exits through an initial public offering (IPO), strategic sale to another company, or secondary buyout to another private equity firm. Successful exits generate returns through debt paydown, EBITDA growth, and multiple expansion.

This process sounds clean and systematic, but the execution is where fortunes are made and lost.

The difference between a 25% IRR and bankruptcy often comes down to how well the team executes operational improvements while managing debt service requirements. Most founders and CFOs never see this level of financial engineering complexity until they're in the middle of it.

LBO financial models form the core basis for any investment decision, entwining company models along with the more sophisticated finance models to calculate the return for the investors. These models demand in-depth knowledge in the fields of finance as well as private equity.

Based on EBITDA multiples, DCF valuations, and market comparables. Entry multiples typically range from 6x to 12x EBITDA, depending on industry, company quality, and market conditions.

2 . Financing Structure:

Detailed debt stack including amounts, interest rates, and amortization schedules. Senior debt usually carries 4-8% interest rates, while subordinated debt and mezzanine financing command 10-15% returns.

3 . Operational Projections:

Five-year financial forecasts incorporating revenue growth, margin expansion, and working capital assumptions. These projections drive cash flow available for debt service and equity distributions.

LBO returns stem from three primary sources that compound over the investment period:

As the company generates cash flow, principal payments reduce total debt, increasing equity value. This deleveraging effect can contribute 30-50% of total returns in successful deals.

Operational improvements and revenue expansion increase absolute EBITDA, directly enhancing enterprise value. Annual EBITDA growth of 5-15% significantly impacts exit valuations.

If the company exits at a higher EBITDA multiple than the entry multiple, this expansion creates additional value. Market conditions and company improvements can drive multiple expansions from entry to exit.

The annualized return measurement that private equity firms use to evaluate deal success. Target IRRs typically range from 15-25% for successful LBOs.

Total cash returned, divided by the total cash invested. Successful LBOs target between 2.0x and 3.0x MOIC over a timeframe of 3-7 years.

Use financial risk-debt measures. The entry level of leverage can range between 4x to 7x EBITDA, but over time, it reduces as the company generates cash flows.

In the context of businesses exploring strategic alternatives, anticipating potential acquisitions, companies should know the value of understanding the concepts of business valuation as well as financial model projections.

The $31.1 billion LBO of RJR Nabisco by Kohlberg Kravis Roberts & Co. remains the most well-known LBO in history, chronicled in the book “Barbarians at the Gate”. This deal showed the size as well as the controversy associated with leveraged buyouts of the 1980s.

The structure involved around 87% debt, leveraging the company's hefty cash flows to finance the massive debt burden. KKR has overcome skepticism to successfully navigate the company through divestitures, cuts, and restructuring before exiting the investment through the IPO route.

Michael Dell teamed up with Silver Lake Partners in a $24.9 billion LBO to make Dell private, thereby taking the computer company out of the capital markets to make it easier for it to change strategies. The deal was largely fueled by debt, totaling about 65%.

The LBO allowed Dell to transform and focus on the enterprise services segment as well as move to the cloud, divest non-profitable consumer businesses. After five years of LBO-driven transformation, the company went back to the market in a rather complex deal related to VMware.

Blackstone Group's $26 billion acquisition of Hilton Hotels represents one of the largest hotel industry LBOs, completed just before the 2008 financial crisis. Even with challenging timing afoot, Blackstone’s patient capital approach and its injected operational improvements were able to generate sustainable returns.

The firm invested in hotel renovations, expanded internationally, and developed new brands while managing debt service through economic downturns. Blackstone's 2013 IPO of Hilton generated one of the most successful private equity exits in history, producing over $14 billion in total returns.

Understanding the benefits and risks of LBO structures helps stakeholders evaluate whether this strategy aligns with their objectives and risk tolerance.

LBOs provide powerful tools for value creation when applied to appropriate targets. The combination of leverage, operational improvements, and private ownership creates conditions for substantial returns that exceed public market alternatives.

Private ownership eliminates quarterly earnings pressures, enabling long-term strategic investments that public companies often avoid. Management teams with significant equity stakes become highly motivated to maximize company performance and value creation.

The leverage that creates LBO return potential also generates substantial risk. Companies must generate sufficient cash flow to service debt obligations regardless of economic conditions or competitive pressures.

Let's be brutally honest here: LBOs work brilliantly when everything goes according to plan, but they can destroy companies when assumptions prove wrong.

The difference between success and disaster often comes down to conservative underwriting and having enough financial cushion to weather unexpected storms. This is exactly why sophisticated financial analysis and experienced leadership become absolutely critical during these transactions.

Successful LBOs require specific target company characteristics and market conditions that align with the leverage-heavy investment strategy. Understanding these criteria helps explain when LBOs make strategic sense.

LBO targets must generate consistent, predictable cash flows sufficient to service debt obligations across economic cycles. Companies with recurring revenue models or defensive market positions often.

2. Strong Market Positions

Market-leading companies, those that enjoy barriers to competition, can maintain pricing power through the periods of operational improvement necessarily involved in LBO ownership.

3. Low Capital Expenditure

The businesses requiring less capital also generate more free cash flow, which can be distributed as equity.

4. Operating Improvement Opportunities

Those that can be quantified in terms of cost-saving potential, revenue-enhancing opportunities, or operational improvements are more than just financial engineering targets.

The firms, which could be publicly traded corporations valued below their intrinsic value, may require private ownership in order to achieve long-term strategies.

Large corporations tend to divest non-core businesses through LBOs so that management can optimize the businesses without the bureaucracy of the corporation.

The management teams in the existing companies form a partnership with the private equity firms to buy the companies.

Financially troubled companies can employ LBO structures in order to recapitalize the company through patient capital.

Sometimes the best LBO targets are not necessarily the fastest-growing companies.

They’re the ones whose boring, predictable cash flows can pay off debt in the good times and the bad. The private equity firms love to buy the profitable widget company rather than the trendy technology start-up, predictability being more attractive when those firms are levered up to 6x.

Understanding how LBOs compare to alternative acquisition approaches helps stakeholders select optimal transaction structures based on their specific objectives and constraints.

Typically, the strategy acquisitions pursued by corporate buyers involve the use of balance sheet cash or equity, excluding the leveraging risk involved in LBOs. The acquisitions emphasize synergies rather than financial restructuring, usually yielding more conservative but viable rates of return.

The corporate buyer can therefore support its higher price structure based upon operating synergies, which financial buyers lack access to. But difficulties in synergy attainment are a potential issue between corporations, due to cultural differences.

Asset purchases represent the procurement of particular assets in a business, as opposed to acquiring the entire company. This process can be ideal in troubled companies, as well as when acquiring particular skill sets.

Asset purchases involve less financing, as well as quicker return generation, but lack the potential for full-spectrum value creation in terms of operating efficiency.

The truth, though, is that every M&A approach has its own set of applications, so it’s essential to choose the most suitable one based on your circumstances.

LBOs are no better, no worse than any other strategy—just a different tool, a different set of potential rewards, risks, consequences. The trick is matching the tool to the job, rather like choosing the right screwdriver for the job.

Organizations planning to explore strategic alternatives should develop financial information and operating statistics that private equity firms require in due diligence. This increases the chances of obtaining a fair valuation while shortening the time it takes to execute the proposed deal.

Working Capital Analysis: Monthly working capital components demonstrating seasonal patterns and operational requirements. Cash conversion cycle optimization opportunities and inventory management practices.

Historical Financial Statements: Audited financial statements over 3-5 years to reflect stable financials, financial consistency, and quality of financial accounts. Monthly financial packages depicting the current financial trends.

Management Projections: Detailed financial plans over 5 years, outlining assumptions regarding revenues, cost structure, as well as capital expenditures. Analyses illustrating the impact of adverse assumptions, like sensitivity analysis, work best.

Customer Concentration: Revenue diversity in the customer base, based upon the terms of the contracts and the retention data. The costs of acquiring customers, as well as the customer lifetime values, for customer accounts in recurring revenue businesses.

Market Position Analysis: Competitive positioning, market share data, and differentiation factors. Pricing power demonstration through historical price increases and customer retention.

Management Team Capabilities: Leadership experience, succession planning, and organizational depth. Strategies for retaining key people, as well as equity incentives.

Understanding financial planning and analysis capabilities and cash flow management becomes essential for companies preparing for potential LBO transactions.

Look,

whether you're considering an LBO as a buyer, seller, or management team, success comes down to having the right financial expertise and operational know-how—capabilities most companies simply don't have sitting around internally.

These deals require leaders who can handle complex debt structures, negotiate favorable terms, drive operational improvements, and guide teams through the inevitable organizational changes that come with new ownership.

The stakes are high enough that trying to figure it out as you go can be an expensive mistake—which is why experienced transaction support often makes the difference between a successful deal and a costly learning experience.

Thinking about a buyout or evaluating strategic alternatives?

McCracken's fractional CFO and interim CFO services help companies build acquisition-ready financial models, evaluate leveraged strategies, and navigate complex transactions, including mergers, acquisitions, and strategic deals with confidence.

From due diligence preparation to post-transaction integration, experienced finance leadership makes these high-stakes decisions work for your specific situation while maximizing value creation opportunities.

Get started with expert transaction guidance →

A leveraged buyout (LBO) is a financial transaction where investors acquire a company using significant borrowed money—typically 60-90% of the purchase price—with the acquired company's assets serving as collateral for the loans.

LBOs are primarily used by private equity firms, often in partnership with existing management teams. Strategic buyers and management teams occasionally structure leveraged transactions independently.

Heavy debt financing means the acquired company must generate sufficient cash flow to cover interest and principal payments regardless of economic conditions. Failure to service debt obligations can lead to bankruptcy.

Ideal targets have predictable cash flows, strong market positions, minimal capital expenditure requirements, and operational improvement opportunities. Stable, profitable businesses with defensive characteristics work best.

LBOs generate returns through three primary drivers: debt paydown using company cash flows, EBITDA growth from operational improvements, and multiple expansion when exiting at higher valuations than entry multiples.

.svg)