Capital budgeting aids businesses in evaluating long-term investments and making smarter financial decisions.

Capital budgeting aids businesses in evaluating long-term investments and making smarter financial decisions.

The conference room falls silent.

The CEO stares at the proposal sitting in front of her: a $5 million facility expansion that promises to double production capacity.

The head of operations swears it's a goldmine.

The sales director claims customers are demanding more inventory. The CFO quietly slides a one-page analysis across the table.

"Based on our capital budgeting analysis," he says calmly, "this investment will destroy approximately $800,000 in shareholder value over the next five years."

The room erupts. How could expanding production capacity—something that sounds so obviously good for business—actually lose money?

Welcome to capital budgeting, where gut feelings go to die and mathematics reveals the truth about long-term investments.

Capital budgeting represents the systematic process companies use to evaluate major investment decisions that will impact their financial performance for years to come.

Unlike day-to-day operational spending, capital budgeting focuses on significant expenditures for assets, projects, or strategic initiatives that require substantial upfront investment but promise future benefits.

The stakes couldn't be higher.

These decisions shape company trajectory, determine competitive positioning, and often represent the difference between sustainable growth and expensive mistakes that haunt balance sheets for years.

Let's jump into the framework that turns capital budgeting from guesswork into strategic advantage

Most business leaders think they understand investment evaluation. "If it makes money, we do it. If it doesn't, we don't." Sounds simple enough—until you realize that "making money" over multiple years involves discount rates, risk adjustments, and cash flow timing that can turn seemingly profitable projects into value destroyers.

Here's what separates successful companies from those that chase shiny objects: disciplined capital budgeting processes that force every major investment to prove its worth using rigorous financial analysis rather than compelling PowerPoint presentations.

Capital budgeting matters because it prevents the expensive mistakes that plague growing companies. That new office lease that seemed reasonable? The manufacturing equipment that promised efficiency gains? The acquisition target with "obvious synergies"? Without proper evaluation, these decisions often become expensive lessons in the difference between what sounds good and what actually creates value.

When facing major decisions like M&A opportunities or infrastructure expansion, capital budgeting provides the analytical framework to separate genuine value creation from emotional decision-making. Companies that master this process consistently outperform peers who rely on gut instinct for major capital allocation decisions.

The most successful CFOs understand that saying "no" to mediocre investments is often more valuable than saying "yes" to seemingly good ones. Rigorous capital budgeting ensures that every dollar deployed has clear, measurable potential for returns that justify the opportunity cost and risk involved.

Capital budgeting techniques provide the mathematical framework for comparing investment opportunities objectively. Each method offers different insights, but smart finance teams use multiple approaches to build comprehensive investment cases—much like how financial planning and analysis requires multiple data points to create accurate forecasts.

Net Present Value calculates the difference between an investment's present value of future cash flows and its initial cost. Positive NPV indicates value creation, while negative NPV suggests the investment destroys shareholder value.

NPV accounts for the time value of money—the principle that $100 received today is worth more than $100 received next year due to inflation and opportunity cost. This makes NPV particularly valuable for comparing investments with different cash flow patterns and time horizons, similar to how cash flow management requires understanding timing and liquidity needs.

Example: A $200,000 software implementation that generates $60,000 annually for five years at a 10% discount rate yields an NPV of approximately $27,500, indicating the investment creates value beyond the required return.

IRR represents the discount rate at which an investment's NPV equals zero—essentially the breakeven return rate. Projects with IRR above the company's cost of capital generally merit consideration, while those below it typically don't.

IRR provides an intuitive percentage return that makes it easier to communicate investment attractiveness to stakeholders. However, IRR can be misleading for projects with irregular cash flows or when comparing investments of different sizes—a common challenge in strategic transactions.

Example: That same $200,000 software implementation might generate a 15% IRR, meaning the investment returns 15% annually—attractive if the company's cost of capital is 10%.

Payback period measures how long it takes to recover the initial investment through generated cash flows. While it ignores the time value of money and cash flows beyond the payback point, it provides a quick risk assessment—shorter payback periods generally indicate lower risk.

This method proves particularly useful for companies focused on working capital management or those operating in uncertain environments where quick capital recovery is essential.

Example: If the software implementation costs $200,000 and generates $60,000 annually, the payback period is 3.33 years ($200,000 ÷ $60,000).

Profitability Index divides the present value of future cash flows by the initial investment, showing how much value is created per dollar invested. PI above 1.0 indicates value creation, while PI below 1.0 suggests value destruction.

PI proves particularly useful when comparing projects of different sizes or when capital allocation strategies involve constrained capital resources—a common challenge for growth-stage companies.

Honestly, no single metric tells the complete story.

Companies that consistently make better investment decisions use multiple techniques to build comprehensive cases rather than relying on whichever method makes their preferred projects look best.

This comprehensive approach becomes even more critical during M&A processes, where sophisticated buyers will evaluate your capital allocation history using all of these methods.

For growing companies that need this level of financial rigor, fractional CFO services provide the expertise to implement disciplined capital budgeting processes without the overhead of a full-time executive.

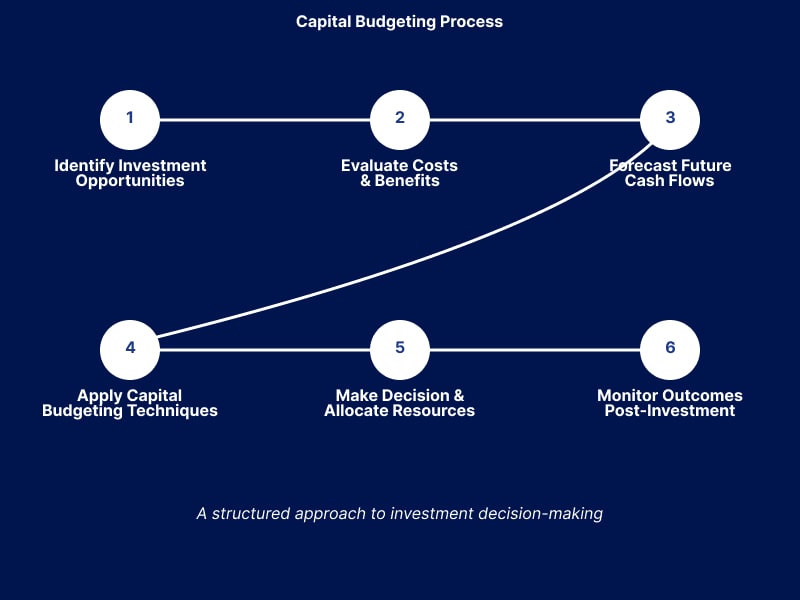

So now that we see some of the best methods in the capital budgeting process, let's go through each step of its implementation.

Effective capital budgeting is just as much a structured process that transforms initial ideas into rigorous investment cases as many other financial processes are.

Each step builds upon the previous one to create comprehensive analyses that support confident decision-making—much like how financial projections require systematic approaches to generate reliable forecasts.

The process begins with opportunity recognition—identifying potential investments that align with strategic objectives and competitive positioning.

Sources include

This step requires the same strategic thinking that drives effective capital allocation strategies.

Comprehensive cost analysis includes initial capital expenditures, ongoing operational expenses, training requirements, and opportunity costs. Benefit evaluation encompasses direct cash flow improvements, cost savings, risk mitigation, and strategic value creation.

Cash flow projections form the foundation of capital budgeting analysis. Focus on incremental cash flows—only those directly attributable to the investment decision.

Include all relevant impacts such as: revenue increases, cost savings, additional expenses, tax implications, and terminal values.

This requires the same rigor that goes into cash flow management for operational decisions.

Next step is to run multiple analysis methods to build comprehensive investment cases. This is financial Scenario Planning at its finest.

Calculate NPV using appropriate discount rates, determine IRR for return assessment, evaluate payback periods for risk analysis, and compute profitability indexes for efficiency comparison—leveraging the methods we covered in the previous section.

The key here is comparing different scenarios: best-case outcomes where revenue projections exceed expectations, worst-case situations where costs overrun or market conditions deteriorate, and most-likely scenarios that reflect realistic operating assumptions.

You’ve got your calculations - time to consider them.

Use analysis results to rank competing investments and make allocation decisions.

Consider both quantitative metrics and qualitative factors like strategic fit, risk tolerance, and resource constraints.

Step 6: Monitor Outcomes Post-Investment

Track actual performance against projections to improve future forecasting accuracy.

Regular monitoring enables course corrections and provides insights for subsequent investment decisions—creating the same continuous improvement cycle that drives effective financial planning and analysis.

All the steps above can create a robust analytical framework, but sometimes the process alone is not enough.

This is where having experienced financial leadership pays massive dividends.

The process sounds straightforward, but each step requires judgment calls that can dramatically impact results.

Which costs are truly incremental?

How do you account for strategic value that's difficult to quantify?

What discount rate properly reflects project risk?

With capital budgeting, the devil really is in the details, and these nuances separate successful investments from expensive mistakes.

Growing companies often struggle with these nuances while juggling daily operations. They end up with analysis that looks sophisticated but misses critical factors that determine actual investment success. A controller or bookkeeper isn't always equipped with the strategic finance expertise these decisions demand.

For companies that need this level of sophisticated analysis without full-time CFO overhead, interim or fractional CFOs provide the experienced judgment necessary to navigate these complex decisions successfully.

Interim CFOs can step in during critical transition periods to lead major capital allocation decisions while fractional CFOs provide ongoing strategic oversight to ensure your investment processes create sustainable competitive advantages.

The best part?

You get what you need, on your dime, on your time. No full-time CFO salary, no equity dilution, no long-term commitments—just the executive-level financial expertise that turns capital budgeting from guesswork into your competitive edge.

Alright, so we've covered the framework and process, but theory meets reality in ways that can devastate even the most carefully constructed models.

Even companies with formal capital budgeting processes make expensive mistakes. Understanding common pitfalls helps avoid the analytical errors that turn promising investments into cautionary tales.

Teams consistently overestimate benefits and underestimate costs, especially for projects they champion. Revenue projections become best-case scenarios rather than realistic assessments. Cost estimates ignore implementation challenges and scope creep.

Companies that consistently generate superior returns build pessimism into their models. They stress-test assumptions, include contingency allowances, and focus on downside scenarios that could derail projected returns—the same disciplined approach that drives effective budgeting and forecasting.

Using inappropriate discount rates can flip investment recommendations. Too low, and value-destroying projects appear attractive. Too high, and worthwhile investments get rejected. Many companies use their overall cost of capital for all projects, ignoring risk differences between initiatives.

Understanding how to properly calculate and apply discount rates requires the same expertise that drives sophisticated investment analysis and valuation decisions.

Relying exclusively on one capital budgeting technique creates blind spots. IRR can mislead when comparing projects of different sizes. Payback period ignores long-term value creation. NPV requires accurate discount rate assumptions.

This tunnel vision mirrors the same analytical errors that plague companies when they focus on single metrics rather than comprehensive financial planning processes.

Continuing investments because of previous expenditures rather than future value creation. "We've already spent $2 million on this system" becomes justification for throwing good money after bad instead of objectively evaluating remaining investment requirements.

Let's talk real scenarios where capital budgeting either saves companies serious money—or reveals that their "great" idea isn't so great after all.

That $3 million warehouse expansion feels like an obvious win until you run the numbers. Factor in permits, utilities, hiring headaches, and the cash you're tying up, and your "slam dunk" might actually lose $400K over five years.

Reality check: Companies doing this right often find that tweaking current operations or partnering strategically beats building new every time.

Going global sounds exciting until capital budgeting shows you the real costs. Currency risk, regulatory compliance, and markets where customers pay when they feel like it can turn your expansion dreams into cash flow nightmares. The companies succeeding internationally? They planned for everything to cost more and take longer than expected—because it always does.

Development costs are just the beginning. Smart capital budgeting forces you to model realistic customer acquisition costs, honest churn rates, and how long before you see actual positive cash flow. The difference between success and burning through your funding? Getting brutally honest about unit economics before you build anything.

ERP vendors promise efficiency gains. What they deliver is budget overruns and operational chaos during implementation. Good capital budgeting asks tough questions: Will those efficiency gains actually happen? What's the real cost when everything slows down during the transition? Smart money budgets 50-100% more than the initial quote and expects benefits to take twice as long.

Every investment you make either strengthens your position or weakens it. Capital budgeting isn't about perfect spreadsheets—it's about making decisions based on reality instead of optimism.

Ready to make smarter investment decisions?

McCracken Alliance's experienced CFOs help growing companies build disciplined capital budgeting processes that actually work. No guesswork, no crossed fingers—just solid analysis that protects your cash and drives real growth. Let's discuss your next big decision!

Capital budgeting is the process companies use to evaluate and select long-term investment projects by analyzing their potential costs, benefits, and financial returns to determine which investments will create the most shareholder value.

The four primary capital budgeting methods are Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, and Profitability Index. Each provides different insights into investment attractiveness and risk.

Capital budgeting prevents costly investment mistakes by providing objective, mathematical frameworks for evaluating long-term projects. It ensures companies allocate limited resources to investments that create the most value rather than those with the most compelling narratives.

Companies use capital budgeting to evaluate facility expansions, technology implementations, market entry strategies, equipment purchases, and acquisition opportunities. Any significant investment requiring substantial upfront costs with multi-year payback periods benefits from capital budgeting analysis.

Capital budgeting focuses specifically on evaluating individual long-term investment projects, while financial planning encompasses broader strategic planning including operational budgets, cash flow management, and overall financial strategy across the entire organization.

.svg)