Discounted cash flow (DCF) is a powerful investment valuation tool. Learn its mechanics, calculation, and strategic importance.

Discounted cash flow (DCF) is a powerful investment valuation tool. Learn its mechanics, calculation, and strategic importance.

The boardroom tension is so thick you could cut it with a knife.

Two investment bankers present vastly different valuations for the same acquisition target:

$50 million versus $120 million.

A $70 million dollar spread?

How can sophisticated financial professionals arrive at such wildly different numbers for the same company?

The answer lies in their valuation methodologies.

One relied on market comparables—essentially what similar companies sold for recently.

The other built a discounted cash flow model that ignored market noise and focused on fundamental value creation.

Guess which approach Warren Buffett uses?

While market-based methods tell you what assets are trading for, DCF reveals what they're actually worth based on their ability to generate cash flows over time.

This isn't just academic theory. DCF drives billions of dollars in M&A decisions, guides venture capital investments, and helps CFOs evaluate major capital projects. Understanding DCF means understanding the mathematical foundation of value creation itself.

Discounted cash flow is a valuation method that calculates the present value of expected future cash flows, adjusted for the time value of money.

Think of it as answering this fundamental question: "If this business generates X dollars of cash flow over the next 10 years, what's that worth to me today?"

The underlying principle behind DCF stems from a simple reality :

Money today? Worth more than money tomorrow.

How come?

Because a dollar in your pocket right now can be invested to earn returns, while a dollar promised next year carries alot of uncertainty and opportunity cost.

The thing about DCF is it cuts through all of the following :

And allows one to focus on intrinsic value—what an asset is fundamentally worth based on its cash-generating ability.

Therefore, DCF really becomes valuable during market volatility, or when comps start swinging wildly based on sentiment rather than fundamentals.

A great example of this is the recent AI and Tech boom, which has been said to be overvaluing some stocks.

For growing companies, DCF provides the analytical framework to evaluate everything from new product launches to acquisition opportunities.

It forces leadership teams to think rigorously about cash flow generation, competitive positioning, and long-term value creation rather than relying on gut instinct or market momentum.

Unlike market-based valuation methods that reflect what investors are willing to pay today, DCF focuses on future cash generation potential.

This forward-looking approach proves especially valuable for evaluating growth companies, emerging markets, or innovative business models where historical comparables provide limited insight.

DCF forces analytical rigor into investment decisions. You can't build a DCF model without explicitly forecasting revenue growth, margin progression, capital requirements, and competitive dynamics. This discipline often reveals assumptions that sound reasonable in presentations but fall apart under mathematical scrutiny.

CFOs use DCF analysis to evaluate major capital projects, ensuring that significant investments actually create shareholder value rather than just increasing company size. The same analytical framework that drives capital budgeting decisions applies to DCF valuation—both require rigorous cash flow forecasting and risk assessment.

M&A teams rely on DCF to determine whether acquisition targets justify their asking prices. When market comparables suggest paying 15x revenue for a SaaS company, DCF analysis can reveal whether that multiple makes sense based on realistic cash flow projections and competitive dynamics.

Startup founders use DCF to prepare for fundraising conversations with sophisticated investors who understand that hockey stick revenue projections mean nothing without underlying unit economics and realistic paths to profitability.

DCF provides a common analytical framework for comparing wildly different investment opportunities. Whether evaluating a new product launch, geographic expansion, or acquisition target, DCF reduces every opportunity to its fundamental value creation potential.

This proves particularly valuable for companies managing multiple capital allocation strategies simultaneously. DCF analysis helps leadership teams allocate limited resources to initiatives with the highest risk-adjusted returns.

The mathematical foundation of DCF valuation is :

PV = CF₁ / (1 + r)¹ + CF₂ / (1 + r)² + ... + CFₙ / (1 + r)ⁿ

Where:

This equation embodies the basic concept that the value of future cash flows decreases with time. The discount rate takes into account the time value and risk involved in realizing the expected cash flow.

In the case of practical DCF models, this equation would contain an expression recognizing the terminal value, where the value beyond the model horizon would be estimated in the following manner:

Enterprise Value = Sum of Discounted Cash Flows + Discounted Terminal Value

The terminal value typically constitutes 60-80% of enterprise value, and hence, its estimation becomes important in obtaining the overall enterprise value.

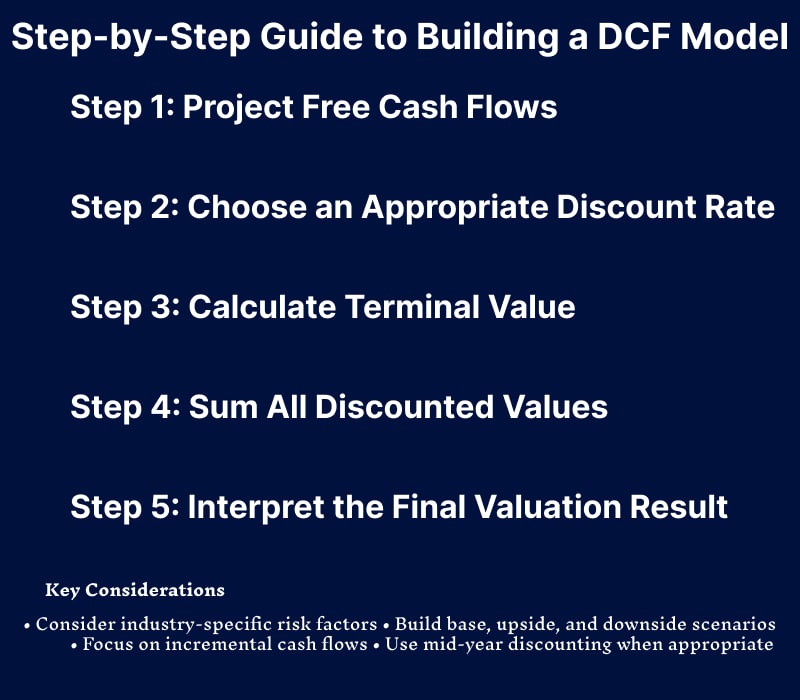

Free cash flow projections form the backbone of any DCF analysis.

First, in reference to the cash flow statement, the concept of free cash flow corresponds to the remaining cash available to all parties after the company has invested in its operations and capital expenditures. In relation to the cash flow statement, the use of the term “free cash flow” provides

Developing accurate cash flow projections means you need to fully understand the cash flow drivers in your industry, such as customer acquisition trends, revenue recognition in your industry, trends in gross margins, and management of working capital. The quality of your cash flow projections affects the quality of your entire valuation.

Typically, most Discounted Cash Flow valuation models have explicitly modeled cash flows ranging from 5-10 years. Technology firms, in general, extend the time horizon in their models in order to adequately model the network effects in their businesses.

The discount rate is the rate that investors demand in order to compensate them for the time value and risk involved in their investment. In the valuation process, the Weighted Average Cost of Capital, a mix of the cost of equity and debt, has commonly been used.

WACC calculation requires several inputs:

Each component reflects different aspects of investment risk and market conditions.

In the case of early-stage businesses and high-risk investments, higher discount rates are used by analysts to factor in higher risks. The risk adjustment ensures that riskier investment opportunities need higher returns in order to remain justified.

Terminal value represents the present value of all cash flows beyond the explicit forecast period. Since businesses often continue operating indefinitely, terminal value typically comprises the majority of total enterprise value.

The most common terminal value calculation uses the Gordon Growth Model:

Terminal Value = Final Year Cash Flow × (1 + g) / (WACC - g)

Where 'g' denotes the long-term rate of growth, usually corresponding to GDP and industry-growth rates. The perpetual growth model must be viewed critically, since even small adjustments in assumptions impact valuations considerably.

The last step discounts all the projected cash flows and the terminal value on the basis of the discount rate chosen.

This present value equation takes the discounted cash flow projections and renders them equivalent in value to present-day investment needs.

The total discounted cash flow values the enterprise, and adjustments can then be made for cash and other items on the balance sheet to derive the equity value for each share.

Begin with revenue forecasts, using reasonable assumptions about the market, the competitive space, and the overall model. Use bottom-up models where feasible, starting with customer base, average revenue per customer, retention, and then pricing.

Convert revenue projections to free cash flows by modeling:

Emphasize cash flows that incrementally accrue to the investment or business, and avoid the typical problem of including overhead costs that would still be incurred even in the absence of the investment.

Calculate the weighted cost of capital for existing businesses using the latest risk-free interest rate, equity risk premium, and industry risk variables. When an organization has plans to optimize its capital structure, use the target capital structure in the cost of capital calculation.

In the case of startups or high-risk projects, equity cash flow discount rates may need to be increased in order to capture the increased uncertainty. Discount factors ranging from 25-40% are commonly employed by Venture Capital firms when making startup equity investments.

Industry-specific risk factors should play a role in discount rate choice. Different discount rates may be appropriate for technology firms than those applied to the utilities industry.

Pick between perpetual growth and the multiple approach when calculating the terminal value. In perpetual growth, the company operates in the future and has a constant growth rate.

Exit multiples essentially assume an ability to sell the company at the available multiples.

In the case of growth companies, perpetual growth can offer better and more stable terminal values than the use of equity multiples, since the equity multiples could remain volatile in the wake of fluctuating stock market conditions.

Discount the projected cash flow in each year using the discount rate. Calculate the total enterprise value by summing the discounted cash flow and the discounted terminal value.

Care should be taken in making assumptions about the timing of the discount. Frequently, mid-year discounting is preferable to year-end discounting, particularly in the case where the company has rather steady cash flow.

The resulting enterprise value can then be compared with other market values, acquisition costs, and investment needed.

Note that in DCF, the model gives you a point estimate, and sensitivity analyses in relation to the major inputs can provide important insights.

Perhaps a framework could be added involving the development of various scenarios, such as the base scenario, upside scenario, and downside scenario, in order to assess the effect of changes in assumptions on their valuations.

Through their assumptions regarding customer acquisition cost, churn, and unit economics, they illustrate the ability of the company's current losses to generate large cash flows on the way to realizing operating leverage.

The DCF model assists in explaining the economic rationale underpinning high revenue multiples, in that the logic related to subscription economics and the marginal cost concept provides valuable cash flow streams once the acquisition process stabilizes.

The strategic buyer in the scenario uses DCF analysis in the evaluation process of the manufacturing company in order to determine the maximum bid price. The methodology takes into consideration synergy, integration costs, and competitive analyses in the process.

The DCF Analysis shows that the target company's 'asking price' corresponds to quite optimistic assumptions regarding the retention of market-share and cost synergy, causing bidders to set 'conservative bids' that help in 'negotiation positioning.'

The $500 million renewable energy development project proposed by the power company undergoes DCF valuation. The approach considers the projections related to the cost of electricity, government regulations, and the efficiencies expected in the proposed development.

Furthermore, the DCF approach provides a basis to compare the proposed investment with other available options and even optimize the manner in which the different projects are financed.

An investment fund uses DCF analysis to screen potential equity investments among mid-cap technology companies. By building consistent DCF models across multiple companies, they identify situations where current market prices diverge significantly from intrinsic value estimates.

This fundamental analysis approach helps identify long-term investment opportunities that market sentiment might be overlooking.

Comparable company analysis (trading comps) values businesses based on multiples of similar public companies. While comps provide market-based validation, they reflect current investor sentiment rather than fundamental value.

DCF offers several advantages over comps: it's forward-looking rather than backward-looking, captures company-specific dynamics rather than industry averages, and provides valuation logic independent of market momentum.

However, comps provide valuable market reality checks for DCF valuations. When DCF analysis suggests a company is worth 3x prevailing market multiples, that divergence demands explanation and additional scrutiny.

The most sophisticated valuation approaches use DCF as the primary methodology while using comps to stress-test assumptions and understand market positioning.

Precedent transaction analysis values companies based on multiples paid in recent M&A transactions. This approach reflects control premiums and synergy values that public market comps might miss.

DCF provides more company-specific analysis than precedent transactions, which reflect deal-specific circumstances, market timing, and buyer-specific synergies. However, precedent transactions help calibrate DCF assumptions about achievable growth rates and margin improvement.

For companies preparing for sale processes, combining DCF analysis with precedent transaction research provides comprehensive valuation frameworks that address both intrinsic value and market realities.

Asset-based valuation methods focus on balance sheet values rather than cash flow generation. These approaches work well for asset-heavy businesses or liquidation scenarios but miss the value created by business operations, customer relationships, and growth opportunities.

DCF captures the full value creation potential of operating businesses, making it superior for evaluating going concerns. However, asset-based methods provide useful downside protection analysis and help establish valuation floors for DCF models.

Understanding DCF analysis provides strategic advantages that extend beyond valuation exercises. The analytical framework forces rigorous thinking about business fundamentals.

You can grow :

CFOs who master DCF analysis make better strategic transaction decisions, avoiding overpaying for acquisitions or underpricing business units during divestitures.

The same analytical rigor that drives DCF valuation improves capital allocation decisions across the organization.

For growing companies that need sophisticated financial analysis without full-time CFO overhead, fractional CFO services provide the DCF modeling expertise necessary for major investment decisions, fundraising processes, and strategic planning initiatives.

Don't let poor valuation analysis cost you millions in missed opportunities or overpaid acquisitions.

Ready to master DCF analysis for your business?

Connect with our team for a complementary consultative conversation and discover how sophisticated DCF modeling becomes your competitive advantage in building long-term value.

Discounted cash flow (DCF) is a valuation method that determines what a business or investment is worth today based on the cash it's expected to generate in the future, adjusted for the fact that money today is worth more than money tomorrow.

The basic DCF formula is: PV = CF₁/(1+r)¹ + CF₂/(1+r)² + ... + CFₙ/(1+r)ⁿ, where PV is present value, CF is cash flow for each period, r is the discount rate, and n is the number of periods.

Use DCF when you need fundamental valuation independent of market sentiment, such as evaluating acquisitions, major capital projects, startup investments, or when market comparables are limited or unreliable.

DCF limitations include sensitivity to assumption changes, difficulty predicting long-term cash flows, terminal value uncertainty, and the challenge of selecting appropriate discount rates. It's only as good as the assumptions that drive it.

DCF accuracy depends on forecast quality and assumption reliability. While precise predictions are impossible, DCF provides valuable analytical frameworks for understanding value drivers and comparing investment alternatives, even when exact valuations prove elusive.

.svg)