Learn what the revenue recognition principle is, how it guides when revenue is recorded, and what the five steps of ASC 606 mean.

Learn what the revenue recognition principle is, how it guides when revenue is recorded, and what the five steps of ASC 606 mean.

A promising SaaS startup just closed a massive three-year enterprise deal worth $3.6 million.

The CEO is ecstatic.

The sales team is out celebrating!

The board is already planning the next funding round based on this "record quarter."

There's just one problem… the eager finance team recorded the entire $3.6 million as Q4 revenue instead of spreading it over the 36-month contract period.

Fast-forward six months to the Series B due diligence process.

Sophisticated investors immediately spot the revenue recognition error.

What looked like explosive growth was actually accounting fiction.

The deal falls apart.

The company scrambles to restate its financials.

The SEC starts asking questions.

All because someone thought revenue recognition was just about when the check cleared.

This is a hypothetical horror story, but it can happen in real life. And it's the kind of expensive mistake that derails promising companies every year.

The revenue recognition principle stands as one of accounting's most critical foundations, dictating when companies should record revenue on their financial statements.

Rather than simply tracking when cash hits the bank account, this principle requires businesses to recognize revenue when it's actually earned—a distinction that fundamentally shapes how financial performance is measured and reported.

This accounting standard serves as the backbone of accrual accounting, ensuring that financial statements accurately reflect business performance by matching revenue with the periods in which the underlying economic activity occurs.

For growing companies, particularly those with complex contracts or subscription models, understanding and correctly applying revenue recognition principles can mean the difference between compliant financial reporting and serious regulatory complications.

So let's dive into the good, the bad, the ugly of Revenue Recognition and how to navigate it without losing your mind (or your margins)

The revenue recognition principle represents a cornerstone accounting standard under Generally Accepted Accounting Principles (GAAP) that establishes when companies should record revenue in their financial statements. The principle mandates that revenue be recognized when earned, regardless of when payment is received, creating a more accurate picture of business performance than simple cash-based tracking.

Under this framework, earning revenue occurs when a company fulfills its performance obligations to customers—delivering goods, completing services, or transferring control of promised assets.

This approach aligns revenue recognition with actual business activity rather than the timing of cash collections, which can vary significantly due to payment terms, customer behavior, or seasonal factors.

The principle operates within the broader accrual accounting system, working in tandem with the matching principle to ensure that revenues and related expenses appear in the same accounting periods. This coordination provides stakeholders with financial statements that accurately reflect the economic substance of business transactions rather than merely their cash flow timing.

Here's where many growing companies hit their first major accounting headache.

They've been running on a cash basis method—revenue happens when the check clears, and expenses get recorded when bills are paid.

It's simple, intuitive, and completely wrong for any business with contracts that span multiple periods, subscription models, or complex delivery schedules.

The shift to proper revenue recognition often reveals that what looked like smooth, predictable growth was actually lumpy performance masked by timing differences.

When companies start recognizing revenue correctly, they sometimes discover their best months weren't as good as they thought, and their worst months weren't as bad. It's an eye-opening moment that separates businesses ready to scale from those still thinking like corner shops.

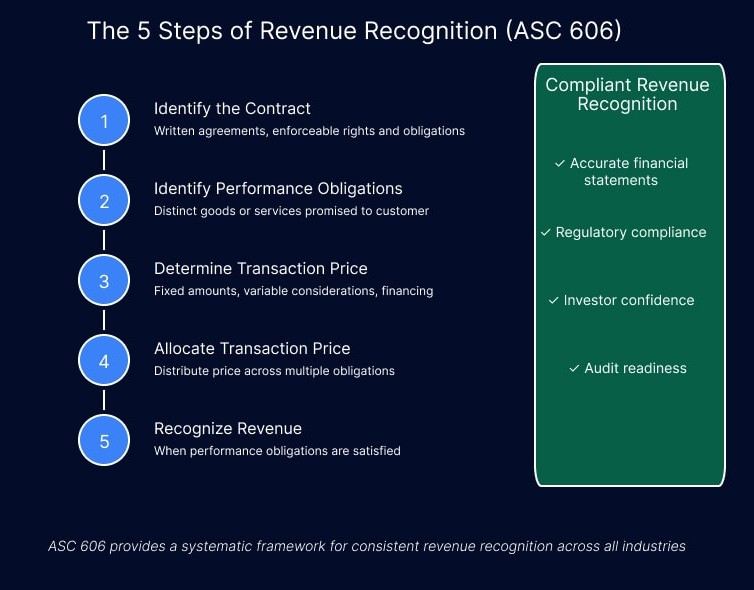

The current revenue recognition standard, codified as ASC 606 under U.S. GAAP, establishes a systematic five-step process for determining when and how much revenue to recognize.

This framework replaced numerous industry-specific guidelines with a single, comprehensive approach designed to improve consistency across different business models and sectors.Step

Contracts form the foundation of revenue recognition analysis. They must be approved by all parties, create enforceable rights and obligations, have commercial substance, and include payment terms that make collection probable. Verbal agreements can qualify as contracts if they meet these criteria, though written documentation provides clearer guidance for complex arrangements.

Performance obligations represent distinct goods or services promised within a contract. Each obligation must be separately identifiable and provide standalone value to the customer. Software companies, for example, might separate licenses, implementation services, and ongoing support into distinct performance obligations requiring different recognition timing.

Transaction price encompasses all consideration the company expects to receive, including fixed amounts, variable payments, and significant financing components. Variable consideration—such as performance bonuses, penalties, or usage-based fees—requires estimation using probability-weighted scenarios or most likely amount methods.

When contracts contain multiple performance obligations, companies must allocate the transaction price based on the standalone selling prices. If observable prices aren't available, companies estimate using cost-plus margins, market comparisons, or residual approaches.

Revenue recognition occurs when performance obligations are satisfied through the control transfer to customers. This can happen at a point in time (product delivery) or over time (service provision), depending on how customers receive and consume benefits.

Real-world application of revenue recognition principles varies dramatically across business models, creating unique challenges for different industries and transaction types. Understanding these variations helps finance teams apply the framework correctly while avoiding common implementation pitfalls.

SaaS companies typically recognize subscription revenue over the service period as they fulfill their ongoing performance obligation. A $12,000 annual software license generates $1,000 monthly revenue recognition, regardless of whether customers pay upfront or quarterly. Setup fees and implementation services may constitute separate performance obligations with different recognition timing.

Construction companies often recognize revenue over time as they satisfy performance obligations through project completion. Progress measurement might use input methods (costs incurred relative to total estimated costs) or output methods (milestones achieved, units delivered). A $2 million office building project that's 40% complete would recognize $800,000 in revenue.

Manufacturing companies selling products with future delivery dates must evaluate when control transfers to customers. If customers gain control upon contract signing (through legal title, payment obligations, and delivery scheduling), revenue recognition occurs immediately. Otherwise, recognition waits until actual delivery and acceptance, which is known as deferred revenue.

Intellectual property licensing creates performance obligations that vary based on license characteristics.

Functional licenses (software access) typically generate revenue over the license period, while symbolic licenses (brand usage) might trigger recognition at the license grant. Royalty arrangements often include variable consideration requiring careful estimation.

The complexity gets real when you're dealing with contracts that don't fit neatly into textbook examples.

Most growing companies discover that their actual customer agreements contain combinations of products, services, implementation support, and ongoing maintenance that require sophisticated analysis to parse into proper performance obligations.

This is exactly why many scaling businesses find themselves scrambling when auditors start asking detailed questions about revenue recognition.

What seemed like straightforward sales suddenly require complex allocation methodologies and judgment calls that can materially impact financial statements.

Having experienced accounting guidance during rapid growth phases prevents these painful surprises during funding rounds or exit processes.

Revenue recognition implementation presents numerous opportunities for errors that can materially impact financial statements and regulatory compliance. Understanding these common pitfalls helps finance teams establish processes that prevent costly mistakes while ensuring accurate reporting.

Timing errors represent the most frequent revenue recognition mistakes. Companies might recognize revenue upon contract signing when delivery hasn't occurred, or delay recognition past performance obligation satisfaction due to a conservative interpretation. Both approaches distort financial performance and can trigger regulatory scrutiny.

Complex agreements often contain ambiguous language about performance obligations, customer acceptance criteria, or payment terms. Misinterpretation can lead to incorrect identification of distinct performance obligations or inappropriate recognition timing. Legal review of contract templates helps establish consistent interpretation frameworks.

Contract modifications, scope changes, or performance obligation adjustments require updated revenue recognition analysis. Companies that fail to reassess recognition patterns when underlying facts change risk accumulating material errors over time. Regular contract review processes help identify necessary adjustments.

Performance bonuses, penalties, usage-based fees, and other variable payments require sophisticated estimation techniques. Companies often underestimate the complexity of probability-weighted scenarios or fail to update estimates as new information becomes available.

Revenue recognition decisions require extensive documentation to support audit reviews and regulatory examinations. Companies with weak documentation practices struggle to demonstrate compliance and may face extended audit processes or regulatory challenges.

Here's what keeps CFOs awake at night: revenue recognition isn't just about getting the accounting right—it's about building systems that can handle complexity as the business scales. The subscription model that works perfectly at $1 million ARR becomes a nightmare at $10 million when you're dealing with hundreds of contract variations, multiple pricing tiers, and customer-specific terms that don't fit standard templates.

Most finance teams underestimate how much operational overhead proper revenue recognition requires. You need robust contract management systems, regular cross-functional reviews between sales and accounting, and sophisticated tracking mechanisms that can handle the inevitable edge cases that crop up in real business situations.

The revenue recognition principle works in close coordination with the matching principle to create comprehensive financial reporting that accurately reflects business performance.

While revenue recognition determines when to record income, the matching principle governs the timing of related expense recognition, ensuring both elements appear in appropriate accounting periods.

Revenue recognition establishes when companies should record income based on performance obligation satisfaction and control transfer to customers. The timing depends on contract terms, delivery schedules, and customer acceptance rather than cash receipt timing.

The matching principle requires companies to recognize expenses in the same periods as the revenues they help generate. This creates logical connections between costs incurred and benefits received, providing clearer pictures of profit margins and operational efficiency.

Together, these principles ensure that financial statements reflect the economic substance of business transactions. A software company recognizing $100,000 in annual subscription revenue should also match the customer acquisition costs, development expenses, and support costs associated with that revenue stream.

However, applying both principles simultaneously can create complexity, particularly for businesses with long sales cycles, multi-year contracts, or significant upfront costs. Companies must carefully track which expenses relate to specific revenue streams and adjust timing accordingly.

U.S. GAAP and International Financial Reporting Standards (IFRS) have achieved substantial convergence in revenue recognition through ASC 606 and IFRS 15, respectively. Both standards adopt the same five-step framework and core principles, though some implementation differences remain relevant for multinational companies.

While the convergence successfully eliminated most major differences, companies operating across jurisdictions must still navigate subtle implementation variations. The differences are relatively minor but can impact specific transactions, particularly in telecommunications, construction, and software industries, where complex arrangements involving multiple deliverables require careful interpretation.

The convergence represents a significant achievement in international accounting harmonization, making it easier for multinational companies to maintain consistent revenue recognition practices across their global operations.

This is where having mature financial processes pays dividends that extend far beyond accounting compliance.

Most growing companies discover that their bookkeeper—however competent at day-to-day transactions—lacks the sophisticated expertise to navigate complex revenue recognition scenarios.

Multi-element contracts, variable consideration, and performance obligation allocation require judgment calls that can materially impact financial statements and investor confidence.

Meanwhile, seasoned CFOs instinctively know how to structure contracts and recognition practices that satisfy both business objectives and regulatory requirements.

They've seen enough deals and audits to anticipate the questions sophisticated stakeholders will ask.

They understand which accounting choices create flexibility and which ones paint you into corners during future transactions—especially critical when fundraising or preparing for strategic exits.

For growing businesses that need CFO-level expertise without full-time CFO overhead, fractional CFO services provide the sophisticated financial leadership necessary to establish bulletproof revenue recognition practices.

These experienced professionals bring decades of experience in complex accounting scenarios, regulatory compliance, and investor relations to companies that require expertise but aren't ready for full-time senior finance executives.

Whether you're a SaaS company scaling rapidly or a traditional business preparing for M&A opportunities, the right financial leadership makes the difference between commanding premium valuations and leaving money on the table.

Revenue recognition isn't just about following rules—it's about building financial infrastructure that supports sustainable growth and successful exits.

When your business needs the expertise to get this right the first time, the seasoned financial executives at McCracken Alliance have guided hundreds of companies through these exact challenges.

Because in the world of sophisticated investors and strategic buyers, your revenue recognition practices don't just tell your financial story—they determine whether anyone believes it.

Ready to bulletproof your revenue recognition practices?

Connect with our team today and discover how proper revenue recognition can become your competitive advantage in fundraising, M&A, and sustainable scaling.

The revenue recognition principle is an accounting standard that requires companies to recognize revenue when it's earned (performance obligations are satisfied) rather than when cash is received, ensuring accurate financial statement representation.

The five steps are: (1) identify the contract with a customer, (2) identify performance obligations, (3) determine the transaction price, (4) allocate the transaction price, and (5) recognize revenue when performance obligations are satisfied.

Under GAAP, revenue should be recognized when a company satisfies its performance obligations by transferring control of goods or services to customers, which may occur at a point in time or over time depending on the contract terms.

Deferred revenue represents cash received before earning revenue through performance obligation satisfaction. It appears as a liability on the balance sheet until the company fulfills its obligations and can recognize the revenue.

Cash basis recognizes revenue when payment is received, while accrual basis (following the revenue recognition principle) recognizes revenue when earned through performance obligation satisfaction, regardless of payment timing.

.svg)