Explore how revenue-based financing works, who it’s right for, and why it’s gaining traction as a flexible, non-dilutive capital solution.

Explore how revenue-based financing works, who it’s right for, and why it’s gaining traction as a flexible, non-dilutive capital solution.

Not every growth plan fits into a venture capital pitch deck—and not every funding round needs to cost you equity. Your cap table doesn't need to look like a United Nations roster of investors, each with their own opinions about how you should run your business.

Revenue-based financing (RBF) is quietly becoming the go-to capital strategy for founders and CFOs who want to scale without sacrificing ownership or taking on rigid debt. Instead of fixed payments or equity dilution, RBF aligns repayment with your actual performance, offering a flexible, founder-friendly path to growth that adapts to the natural rhythms of your business.

So if you thought debt and equity financing were the only options for funding growth, read on to discover how revenue-based financing offers a third path that addresses many of the limitations of traditional funding, while creating its own unique trade-offs worth understanding.

Revenue-based financing represents a fundamental shift in how growth capital works. Rather than demanding a slice of your company or locking you into fixed monthly payments regardless of performance, RBF providers advance capital in exchange for a percentage of your monthly revenue until a predetermined cap is reached.

The structure typically involves:

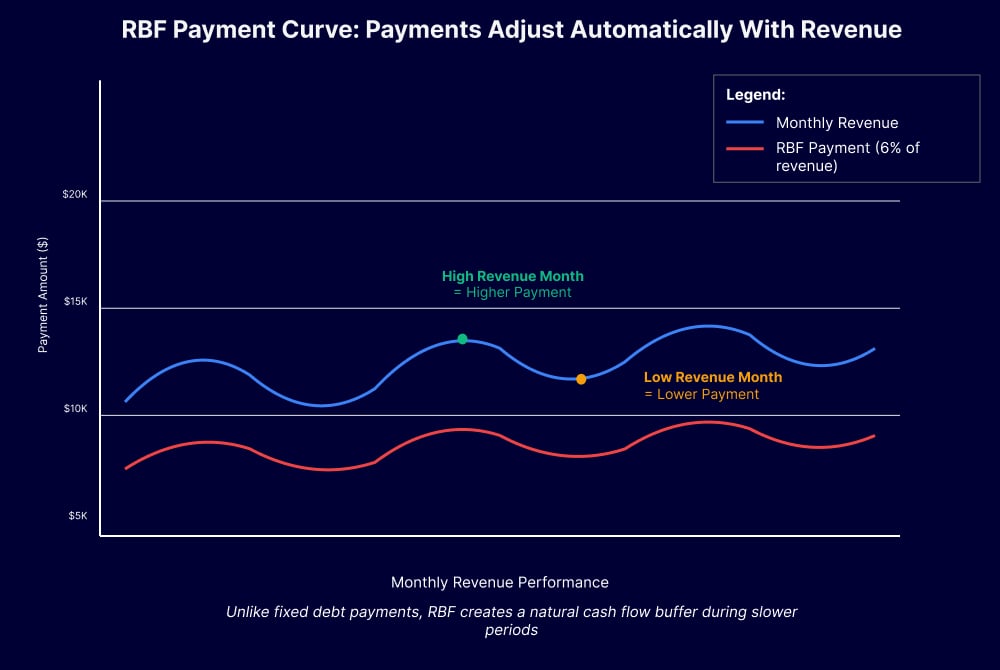

This creates a repayment model that ebbs and flows with your business performance: higher revenue months mean larger payments, while slower periods naturally reduce your repayment burden.

This financing model was designed specifically for businesses with predictable, recurring revenue streams.

SaaS companies, subscription-based services, e-commerce brands with strong repeat purchase patterns, and direct-to-consumer businesses with demonstrated revenue consistency find RBF particularly attractive.

The key differentiator lies in the alignment of interests—your capital provider succeeds when your business succeeds, creating a partnership rather than a creditor relationship.

Unlike traditional debt, RBF doesn't require perfect credit scores or substantial collateral. Instead, providers focus on revenue stability, customer retention rates, and gross margin health. This shifts the underwriting conversation from backward-looking creditworthiness to forward-looking business fundamentals.

Here's the thing about RBF: it's actually pretty simple once you strip away the jargon.

You get money now, you pay it back as a percentage of revenue later.

No board meetings, no dilution drama, no personal guarantees.

Just performance-based payments that ebb and flow with your business.

The mechanics of RBF are refreshingly straightforward, though the implications require careful consideration. Once approved, you receive capital upfront, typically ranging from $50,000 to several million dollars, depending on your revenue scale and the provider's risk appetite.

The core structure involves three moving parts:

The repayment structure creates a natural performance-based curve. During strong revenue months, you'll pay more toward the balance, accelerating your path to full repayment.

Conversely, if revenue dips—whether due to seasonality, market conditions, or temporary setbacks—your payments automatically decrease, preserving cash flow when you need it most.

Here's a practical example that shows how this works in practice: Imagine borrowing $500,000 with a 6% revenue share and a 1.5x repayment cap, meaning you'll ultimately pay back $750,000.

Month 1: Your MRR hits $200,000 → Your payment: $12,000

Month 3: Revenue grows to $300,000 → Your payment: $18,000 (paying off faster!)

Month 8: Seasonal dip to $150,000 → Your payment: $9,000 (automatic breathing room)

The beauty: No renegotiation, no covenant violations, no emergency board calls. The payment just adjusts automatically.

RBF providers typically evaluate several key factors during underwriting, but forget perfect credit scores and three years of tax returns. They focus on forward-looking metrics that actually predict repayment ability:

✓ Revenue Consistency: 12-18 months of stable or growing revenue

✓ Low Customer Churn: Proof that customers stick around

✓ Healthy Gross Margins: Usually 70%+ for SaaS, varies by industry

✓ Predictable Patterns: Seasonal businesses are fine if the seasonality is predictable

✓ Strong Unit Economics: Clear path from revenue to profitability

They're particularly interested in businesses that can demonstrate predictable revenue patterns and strong unit economics rather than backward-looking credit history or personal guarantees.

Traditional lenders want to see three years of profitable tax returns and perfect credit, while VCs want hockey stick growth and a path to billion-dollar valuations.

RBF providers? They just want to see that you're building a real business with real revenue that solves real customers' real problems. It's refreshingly practical.

Like any financing option, RBF isn't a magic bullet—it solves specific problems while creating others. Before you get swept up in the "no dilution" excitement, let's break down what you're actually signing up for.

RBF allows founders to retain full ownership and control without giving up equity or board seats. Unlike equity financing, there are no preference stacks, liquidation preferences, or investor governance requirements that can complicate future business decisions.

Repayment automatically adjusts based on your revenue performance. During strong months, you pay more and accelerate repayment. During slower periods, payments decrease naturally, providing breathing room when cash flow is tight.

RBF providers typically close deals within 4-8 weeks, significantly faster than venture capital rounds (6-12 months) or traditional bank loans (2-6 months). This speed advantage becomes crucial when market opportunities emerge or competitive pressures demand rapid response.

Unlike traditional debt, RBF doesn't require perfect credit scores or substantial collateral. Providers focus on revenue stability and business fundamentals rather than backward-looking credit history or personal guarantees.

For founders concerned about giving up ownership or dealing with aggressive debt covenants, RBF provides a middle ground that preserves control while accessing growth capital without the restrictions of traditional debt agreements.

The effective cost of capital for RBF typically ranges from 15-35% annually, significantly higher than traditional bank loans (5-15%). While more expensive than debt, it often costs less than equity dilution when calculated over the long term.

Even though payments adjust with revenue, they never disappear entirely. Companies with highly seasonal or unpredictable revenue patterns may struggle with percentage-based payments during extended low-revenue periods.

RBF is most suitable for businesses with consistent, recurring revenue streams like SaaS companies, subscription services, or e-commerce brands with repeat customers. Companies with lumpy or project-based revenue may find RBF challenging.

Some providers include origination fees, minimum payment floors, or automatic renewal clauses that can complicate the seemingly straightforward percentage-based structure. Understanding all terms becomes crucial before committing to any RBF agreement.

RBF shines in specific strategic scenarios where traditional funding falls short. Product launches or market expansion initiatives often require capital before revenue validates the investment, but after you've demonstrated core business viability. RBF bridges this gap perfectly, providing growth capital without the extended timeline of equity raises.

Here's where we see smart CFOs make the RBF move: extending runway before a major equity round. Instead of raising Series A at a lower valuation during unfavorable market conditions, companies use RBF to fund 12-18 months of additional growth, potentially doubling or tripling their valuation for the eventual equity round. The RBF cost becomes insignificant compared to the dilution savings.

Seasonal businesses find RBF particularly valuable for smoothing cash flow gaps. Rather than maintaining large cash reserves or struggling through slow periods, the automatic payment adjustments help maintain operations while preserving capital efficiency.

Paid growth campaigns with demonstrable return on investment represent another ideal RBF use case. When you can reliably generate $1.50 of revenue for every $1.00 of marketing spend, RBF provides the fuel to accelerate these proven channels without waiting for traditional financing approval processes.

Companies approaching profitability but not quite there yet often find RBF fills the gap perfectly. Traditional lenders want to see consistent profitability, while VCs may view near-profitable companies as too mature for early-stage funding but too small for growth equity. RBF providers focus on revenue trends rather than bottom-line profitability, making them ideal partners for this transition period.

Revenue-based financing works best for companies with predictable revenue streams seeking flexible, non-dilutive capital.

The effective cost typically ranges from 15-35% annually, but with no dilution and payment flexibility.

Timeline to funding: 4-8 weeks. Founder control remains intact, with no board seats or governance changes.

Equity Financing suits companies with massive growth potential seeking significant capital and strategic partnerships.

While dilution can be substantial (15-25% per round), the capital is typically larger and comes with valuable expertise and networks.

Timeline: 6-12 months. Founders accept governance changes and board oversight in exchange for patient capital and strategic support.

Traditional Debt offers the lowest cost of capital (5-15% annually) but requires strong credit, collateral, and proven profitability. Fixed payments regardless of performance create both predictability and inflexibility.

Timeline: 2-6 months. Personal guarantees and restrictive covenants often accompany traditional debt.

Smart capital strategies often combine elements from each category.

Companies might use RBF to extend runway before an equity round, leverage traditional debt for equipment purchases, and maintain a working capital line of credit for operational flexibility. The key lies in matching the capital source to the specific use case and timing requirements.

For founders feeling overwhelmed by these choices—and honestly, who isn't?—this is exactly where fractional CFO expertise becomes invaluable. Having someone who's navigated these waters before, who understands the subtle differences between provider terms and can model the long-term implications, often pays for itself in the first financing decision alone.

The decision to pursue revenue-based financing shouldn't be made in isolation. Like any capital strategy, RBF requires careful analysis of your specific situation, growth plans, and alternative options.

Start by honestly assessing your revenue predictability. RBF providers want to see consistent month-over-month growth with manageable churn rates. If your revenue swings wildly or depends heavily on one-time transactions, RBF may not be the optimal choice.

Model the repayment scenarios under different revenue growth assumptions. Use financial projections to model your repayment timeline before committing to any RBF structure. Understanding how payments would impact cash flow during both growth and contraction scenarios helps avoid unpleasant surprises.

Consider the timing within your broader capital strategy. RBF can offer strategic capital without diluting long-term allocation flexibility, but it works best when integrated thoughtfully with your overall funding roadmap.

Pay attention to recurring revenue and gross margin—key metrics RBF providers analyze. Strengthening these fundamentals before approaching RBF providers can improve terms and increase approval odds.

Finally, remember that you can use RBF to extend runway without increasing your burn multiple. This becomes particularly powerful when market conditions make equity financing less attractive or when you're approaching key milestones that will improve your valuation.

Revenue-based financing represents more than just another funding option—it's a strategic tool that, when used appropriately, can accelerate growth while preserving founder ownership and maintaining operational flexibility. The key lies in understanding when it fits your specific situation and how it integrates with your broader capital strategy.

Most founders discover RBF when they're already deep in funding conversations, scrambling to compare options under time pressure. Getting ahead of this decision—understanding your options before you need them—gives you the luxury of strategic choice rather than reactive scrambling. Sometimes the best financial strategy is simply having a strategy at all.

Ready to build a financing strategy before you need it?

McCracken Alliance connects you with fractional CFO expertise that can guide you through complex capital decisions and help you evaluate what makes sense for your specific situation.

Revenue-based financing is a funding model where businesses repay borrowed capital through a percentage of monthly revenue rather than fixed payments, with repayment continuing until a predetermined multiple of the original amount is reached.

Unlike traditional loans with fixed monthly payments regardless of business performance, RBF payments fluctuate with revenue—higher revenue months mean larger payments, while slower periods automatically reduce payment obligations.

RBF works well for startups with predictable recurring revenue streams, particularly SaaS companies, subscription businesses, and e-commerce brands with demonstrated revenue consistency and healthy gross margins.

Pros include no equity dilution, flexible payments tied to performance, faster approval than traditional financing, and no personal guarantees. Cons include higher effective cost than traditional debt and potential cash flow pressure if revenue percentages are too high.

Repayment is calculated as a fixed percentage (typically 3-8%) of monthly recurring revenue, continuing until you've repaid a multiple (usually 1.3x-1.6x) of the original borrowed amount, creating automatic payment adjustments based on business performance.

.svg)