Compare C Corps and S Corps to determine the best fit for your business. Learn about tax implications, ownership rules, and investor access.

Compare C Corps and S Corps to determine the best fit for your business. Learn about tax implications, ownership rules, and investor access.

When to form a C Corp or an S Corp is one of the most important decisions a businessman makes, but a lot of folks think of this as a mere tax dodge.

It is much, much more complex than that.

Your choice has a bearing on nearly all areas, such as who can invest in your business, distributing profits, obtaining funding, and finally, your departure or transferring ownership.

While both provide you with liability protection and authenticity since you're officially incorporated, they differ vastly on taxation, ownership, and other matters.

Understanding these differences is much more than a matter of maximizing your tax savings now; it’s about creating a foundation that aligns with your goals.

A C Corporation represents the default corporate structure that most people envision when they think of "incorporating a business."

It's a separate legal entity that can own assets, enter into contracts, and assume liabilities independently of its owners. C Corps provide complete liability protection for shareholders and offer maximum flexibility in terms of ownership structure, profit distribution, and capital raising strategies.

An S Corporation, by contrast, isn't actually a different type of corporation at all—it's a tax election that qualifying businesses can make with the IRS.

Any corporation that meets specific eligibility requirements can elect S Corp status by filing Form 2553, fundamentally changing how the business gets taxed while maintaining the same corporate legal structure and liability protections.

This is a massive distinction because it relates to every aspect of a company’s operations.

Both require formalities of incorporation, such as filing articles of incorporation, creating bylaws, appointing directors, and attending to corporate formalities such as annual meetings of the board.

Activities from day to day aren't that different, but where you're headed—and what your customers, investors, or businesses want—means your implications can differ greatly.

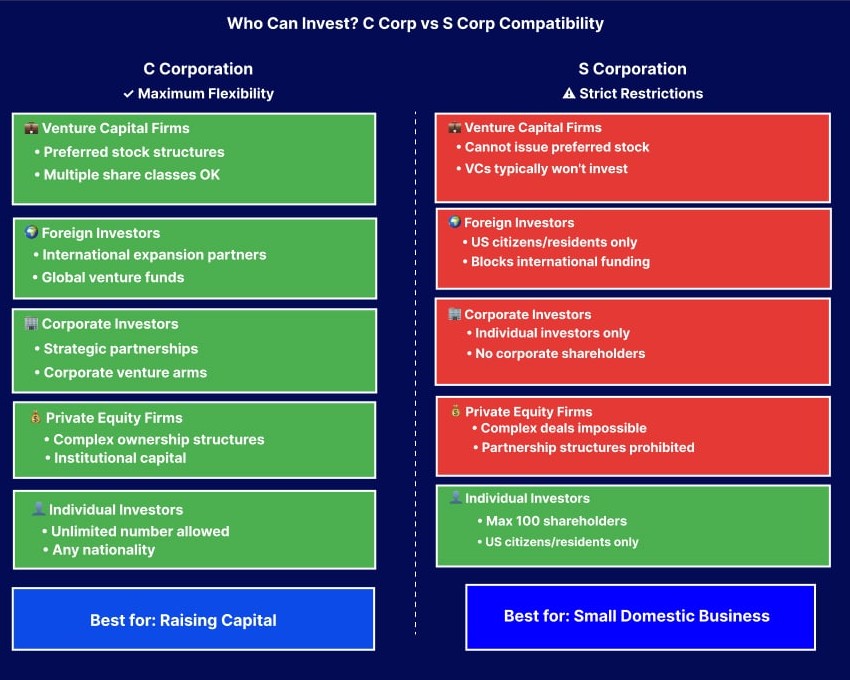

The ownership restrictions create perhaps the most practical difference between C Corps and S Corps, directly impacting your ability to raise capital and scale your business.

These limitations aren't just technical details—they fundamentally shape your strategic options and growth trajectory.

The S Corps have strict shareholder limits, and these can really be a hindrance to expansion.

The IRS limits the number of shareholders for S Corps to 100, and all of these must be United States citizens or residents.

This means that there can be no foreign investors, corporations, partnerships, or trusts other than a few trusts that can own shares of S Corp stocks.

Additionally, there can only be one class of stock for an S Corp.

C corporations can be owned by basically anyone.

They can have as many shareholders as possible, get money from corporations as well as large institutions, and also have multiple classes of stock.

This can be important if you require multiple means of financing or if you want to implement equity participation programs for key employees.

You can see where this is going if you think about growth. It’s possible that a tiny professional services firm, say a company with three local partners, could be just fine as an S Corp.

They get the pass-through tax benefits, and they keep under the cap. But a tech startup trying to bring on VC money?

Game over, unless you can switch to being a C Corp. Venture capitalists want preferred stock, and they want to be able to tap foreign money—options that only C Corps provide.

These ownership rules also affect succession planning and exit strategies.

Shareholders of S Corps must deal with numerous constraints if they want to sell to strategic buyers or private equity, especially if these buyers include foreign companies or corporations.

Then, there are LBO transactions that come bundled with complicated ownership structures and multiple classes of investors that violate the rules for being an S Corp. In these situations, a switch to being a C Corp or working through the underlying LLC is required.

Understanding ownership interests is especially important when these rules might limit your future course of action or reduce the value of your business.

The difference in taxation for C Corps and S Corps is what really catches people’s attention, but what makes the differing rules so tricky is that choosing the better structure is about more than just taxation.

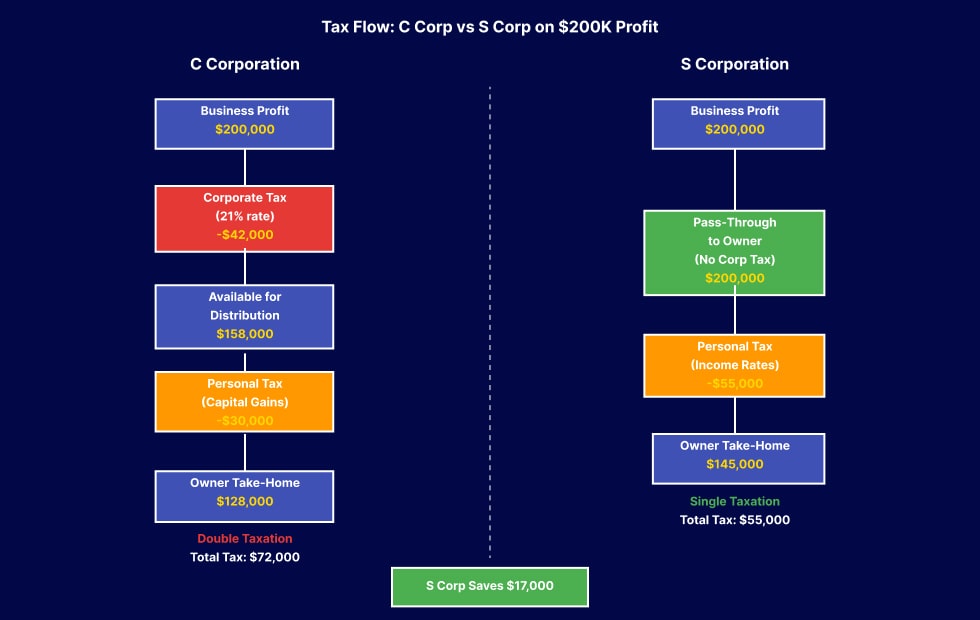

Consider a profitable consulting business generating $200,000 in annual profits with one owner-operator:

The taxation of C corporations provides a number of advantages that most entrepreneurs fail to take advantage of. One of these is that money can be retained without the company's stockholders being charged taxes.

An S Corporation eradicates the problem of double taxation, where the corporation's income is taxed. Instead, the corporation's income, whether profits or losses, is directly reported on the taxpayer's return.

The IRS examines the extent of the pay to make sure that the pay is ‘market rate’ for the type of work being done, to keep a business owner from dodging payroll taxes by paying himself minimal pay and high distributions.

When referring to attracting investments from the outside world, the advantages that C corporations have over other corporations are far-reaching to the extent that C corporations can be said to be the almost universal choice for institutions looking to invest in businesses.

Venture capital firms, private equity investors, and institutional funds typically require preferred stock structures that provide liquidation preferences, anti-dilution protection, and enhanced voting rights.

These provide protection for both parties for the downside but lack protection for stock classes, making them unfeasible under the rules of the S Corp.

Furthermore, most institutional investors can be corporations, partnerships, or even have foreign limited partners. They aren’t allowed to own shares of an S Corp.

The Delaware C Corporation has become the gold standard for venture-backed startups precisely because it provides the legal framework and investor familiarity that facilitates efficient capital raising.

Delaware corporate code provides mature case laws for intricate transactions, advanced corporate structure, and shareholder protection that may be unavailable or less developed elsewhere.

Venture capital companies largely decline to invest in anything other than Delaware C Corps, thus making this structure a requirement for businesses that seek institutional investments.

Fundraising for startups often requires multiple investment rounds with increasingly complex terms and valuations.

C Corps can address these requirements through the creation of multiple classes of stock, conversion mechanisms, and a structure that aligns the interests of investors and founders.

S Corporations, by contrast, work well for businesses that can fund growth through retained earnings, bank financing, or small groups of domestic individual investors.

Professional services firms, local retail businesses, and family-owned enterprises often thrive with S Corp structures because they rarely need the complex capital structures that institutional investors require.

It’s a limitation that is not only confined to the world of venture capital but also to the world of strategic

When corporations strategize for a possible acquisition or initial public offering, prospective buyers tend to favor C Corp structuring.

Converting from an S Corp to a C Corp is possible, but it creates timing considerations and potential tax complications that can complicate transaction execution.

Both C Corps and S Corps require substantially more administrative overhead than simpler business structures, but the specific compliance requirements differ in ways that affect ongoing operational costs and complexity.

Universal Corporate Requirements: All corporations must maintain formal governance structures, including bylaws, regular board meetings, annual shareholder meetings, and detailed corporate records.

They need federal tax identification numbers, must file annual reports with state authorities, and should implement consistent financial reporting practices that document corporate activities and decisions.

The S Corporations increase the complexity of corporate laws to a high extent.

The initial S Corp election requires filing Form 2553 with the IRS within specific timeframes, and maintaining S Corp status requires ongoing monitoring of shareholder eligibility.

They must monitor the status of shareholder citizenship, keep up-to-date on the 100-shareholder limit, and make sure that share ownership is limited to legally permitted parties. It can result in the loss of S Corp status, and this can be a serious matter from a taxation aspect.

The payroll tax obligations of the owner-employees of an S Corp generate compliance risks that businesses tend to underestimate.

Determining "reasonable compensation" requires market research and documentation, particularly for owner-operators who might prefer to minimize W-2 wages in favor of distributions.

The IRS increasingly audits S Corp compensation levels, making professional guidance essential for businesses with significant profits relative to owner compensation.

For S Corps that have multiple shareholders, accurate K-1 preparation and distribution can become quite expensive and complicated.

Both models require expert advice to effectively cope with the compliance process and minimize compliance risks. Most businesses may require the help of a fractional CFO who is experienced in tax matters to give them the advice they need to cope with corporate compliance.

The mechanics of profit distribution create some of the most practical differences between C Corps and S Corps, directly affecting cash flow management, tax planning, and owner compensation strategies.

C Corp distributions are driven by simple rules, but these result in taxation complexity.

The company is able to make profits that can be accumulated for as long as the company wants without being taxed.

When the company actually distributes its profits, dividends enjoy preferential tax rates of up to a maximum of 23.8% for high earners.

However, the distributions that corporations make must be made pro rata to all members of a particular class of shareholders. This creates a challenge for closely-held corporations where the shareholders have contributed different levels of time, money, or skills to the business.

In S corporations, profits are allocated to shareholders automatically according to their ownership percentage, regardless of whether such profits require actual cash.

Indeed, this pass-through taxation system requires that the stockholders pay personal income tax for their respective proportion of corporate profits, even without actually receiving dividend payments for such purpose.

Cash flow management is central to the management of Smart S Corp, as the company requires cash distributions to satisfy its tax liability.

The reasonable compensation requirement for S Corp owner-employees creates both opportunities and complexity.

The owner-employees must be issued W-2 wages that fairly value their work prior to making distributions.

It is a safeguard against abuse but entails continuous evaluation of benchmarking of compensations. It also sidesteps payroll taxes such as Social Security and Medicare taxes, offering a possible tax advantage of 15.3% for gains distributed.

Consider a profitable S Corp with $300,000 in annual profits and one owner-operator. If reasonable compensation equals $100,000, the owner receives $100,000 in W-2 wages (subject to payroll taxes) plus $200,000 in distributions (avoiding payroll taxes). This structure can save approximately $30,600 in payroll taxes compared to taking the entire amount as salary.

Both structures require sophisticated planning around working capital needs, seasonal cash flows, and tax distribution requirements.

The decision framework becomes clearer when viewed through specific business scenarios and growth objectives.

You can select C Corp if you intend to:

Technology start-ups, venture-capitalized businesses, or businesses that have a complex ownership structure almost surely qualify for C Corp flexibility.

Use the S Corp structure if you:

Professional corporations, family businesses, or owner-operated businesses tend to flourish under the structure of an S Corp, especially if these businesses accumulate regular profits, paying them out to their owners.

These strategic implications are of a long-term nature and include issues of exiting the country.

C Corps provide maximum flexibility for future transactions but create current tax inefficiencies for distributed profits. S Corps optimize current tax treatment, but may limit future strategic options or require costly conversions before major transactions.

Here's what most articles won't tell you:

The "best" choice often depends less on tax rates than on your specific growth trajectory, capital requirements, and exit timeline.

A profitable consulting firm might save $15,000 annually with S Corp status, but if that firm eventually wants to sell to a strategic acquirer or private equity firm, the S Corp restrictions could cost hundreds of thousands in reduced valuation or transaction complexity.

Not necessarily true. For businesses that retain significant earnings, C Corp status can provide tax advantages through lower corporate rates and deferred personal taxation. Additionally, very high-income S Corp shareholders may face higher personal tax rates than corporate rates, making C Corp status more attractive.

Completely false. S Corps can revoke their election and become C Corps relatively easily, though timing considerations affect tax implications. C Corps can elect S Corp status if they meet eligibility requirements, though built-in gains taxes may apply for a transition period.

Wrong again. Many small businesses benefit from a C Corp structure when they need investment flexibility, plan to retain earnings, or want to implement sophisticated employee benefit programs. The structure scales effectively from single-owner businesses to multinational corporations.

False. S Corps must maintain the same corporate governance requirements as C Corps, including board meetings, bylaws, and corporate resolutions. The S Corp election changes taxation, not corporate legal requirements.

This really oversimplifies what a complex calculation is. It's a black and white thinking that can allow you to miss the true benefits of a C corp. For a business that reinvests profits, rather than distributes them, C corporations provide tax advantages.

Additionally, qualified small business stock can provide significant capital gains exclusions that offset double taxation concerns.

Understanding these realities helps business owners make informed decisions based on their specific circumstances rather than generic advice or oversimplified tax comparisons.

The C Corp vs. S Corp choice is much more than a taxable election; rather, this is a choice that permeates every aspect of your business development, from day-to-day activities to your long-term exit strategy. Both options provide a host of benefits, but these models suit different business models and different paths of development.

The most successful entrepreneurs understand that optimal entity structuring is a matter of weighing short-term tax optimization techniques against long-term flexibility.

Seeking professional advice on this process can keep your initial business structure choice from working against your long-term goals.

Your business's capital needs, expansion plan, ownership, and plan for exiting the business must be considered when weighing these alternatives. Businesses that require institutional investments, enter foreign markets, or retain profits usually find the flexibility offered by a C Corp structure acceptable, even at a short-term tax expense. Net-profit, closely held businesses owned by people from your country of residence, structurally optimize taxes for efficiency through the S Corp election.

The complexity of entity selection, tax planning, and strategic structuring often benefits from experienced professional guidance. Whether you need help with business succession planning, cash flow optimization, or a comprehensive financial strategy, having advisors who understand both the technical requirements and strategic implications can make the difference between a structure that supports your goals and one that creates unexpected limitations.

When you're weighing entity choices, evaluating tax strategies, or planning for growth and investment, having someone who's guided businesses through these decisions can provide the clarity and confidence you need to make the right choice for your specific situation.

McCracken's CFO network regularly helps business owners evaluate entity structures, optimize tax strategies, and build frameworks that support long-term success.

Talk to an advisor to explore how professional guidance can help you choose the right corporate structure and develop tax-efficient strategies that align with your business objectives and growth plans.

The main difference is found in taxation and ownership limitations. When a C Corp is created, the corporation is subject to double taxation. However, there is no limit to the number of stockholders, and ownership can be structurally flexible. Although the S Corp is exempt from double taxation because of pass-through taxation, its ownership is limited to 100 United States citizens, and only one class of stock is allowed.

S Corps provide a possible overall tax saving because of pass-through taxation and the payroll tax advantage, although a C Corp may be beneficial to a business that retains its profits or when in lower tax brackets.

Yes. A C Corporation can elect S Corp status by filing Form 2553 if it meets IRS eligibility requirements, though built-in gains taxes may apply during a transition period for appreciated assets.

S Corps can issue stock, but only one class and only to eligible shareholders (U.S. citizens/residents, maximum 100 shareholders, no corporate or partnership owners). This significantly limits investment options compared to C Corps.

C Corps work well for small businesses planning to raise capital, retain earnings, or eventually scale significantly. However, S Corps often provide better tax efficiency for profitable, owner-operated small businesses that don't need complex ownership structures.

.svg)