When investors scan a balance sheet, they often focus on assets, debt levels, or cash positions. But there's one line item that tells a more complete story about a company's financial health and strategic direction:

Retained Earnings.

Retained Earnings are the portion of a business's profits that are not distributed as dividends to shareholders, but are instead reserved for reinvestment back into that business.

This often-overlooked metric reveals whether a business consistently generates profits, how management prioritizes growth versus shareholder distributions, and what kind of financial foundation exists for weathering storms or seizing opportunities.

Unlike flashy revenue numbers that dominate earnings calls, retained earnings accumulate quietly over time, building a financial fortress from reinvested profits.

Every dollar sitting in retained earnings represents a choice—management decided this money would create more value inside the company than in shareholders' pockets.

The companies that master this balance between immediate returns and long-term reinvestment often separate themselves from competitors who either hoard cash ineffectively or distribute profits without building sustainable competitive advantages.

Retained earnings function as the company's internal savings account or ‘sinking fund’. They represent the portion of net income that management decides to keep within the business rather than distribute to shareholders as dividends.

At base, a company’s goal is to generate profits, and it often reports to the shareholders on that profit. However, without retained earnings, there would be no funds to reinvest to make the business better.

Retained earnings are like the food your body stores as energy reserves.

When you eat, you don't immediately burn every calorie - your body stores some as glycogen and fat to fuel future activities, growth, and essential functions.

A company faces the same choice your body does:

It can "consume" all its profits immediately by paying them out as dividends (like burning every calorie as soon as you eat), or it can store some of that energy as retained earnings to power future growth and operations.

Just as your body needs stored energy to:

A company needs retained earnings to:

And here's the key parallel: both stored body energy and retained earnings aren't "wasted" resources.

The energy your body stores today enables better performance tomorrow.

Similarly, the profits a company retains today should generate even greater returns - and potentially larger dividends - in the future.

A company that pays out every penny of profit is like someone who burns every calorie immediately - they might feel good in the short term, but they'll lack the reserves needed for growth and resilience.

Unlike cash, which represents immediate liquidity, retained earnings reflect the cumulative reinvestment decisions made by management over the life of the company, creating a historical record of how profits have been allocated between shareholder distributions and business growth.

This metric serves multiple strategic purposes within an organization's financial framework.

Retained earnings fund growth initiatives without requiring external financing, provide a financial cushion during challenging periods, enable debt reduction to improve the balance sheet, and create flexibility for opportunistic investments or acquisitions that might arise.

Companies that thoughtfully manage retained earnings can fund expansion without diluting ownership through equity raises or taking on debt that increases financial risk.

This self-funding capability becomes particularly valuable during economic downturns or when external financing becomes expensive or unavailable.

Retained earnings occupy a specific position within the shareholders' equity section of the balance sheet, typically listed after share capital and additional paid-in capital but before other comprehensive income or treasury stock adjustments.

This placement reflects their nature as internally generated equity rather than capital contributed by external investors.

The retained earnings balance grows over time with profitable operations, as each period's net income (minus any dividends paid) accumulates to increase this equity component.

Unlike assets or liabilities that can fluctuate based on operational decisions, retained earnings provide a running total of all profitable periods minus all losses and dividend distributions throughout the company's history.

However, retained earnings can indeed become negative, creating what accountants term an "accumulated deficit."

This situation occurs when cumulative losses exceed cumulative profits, often seen in early-stage companies burning cash to establish market position, mature companies facing industry disruption, or businesses recovering from significant one-time write-offs or impairments.

Most entrepreneurs don't realize that negative retained earnings aren't necessarily a death sentence—they're often a normal part of the growth journey.

The key is understanding whether negative retained earnings result from strategic reinvestment or operational problems that threaten long-term viability.

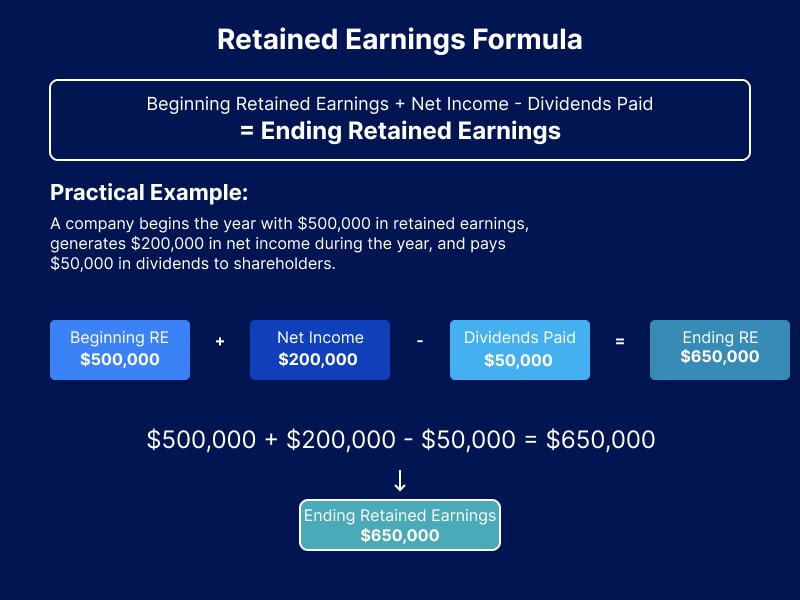

The retained earnings calculation follows a straightforward formula that tracks how profits flow into the company's accumulated equity over each reporting period:

Beginning Retained Earnings + Net Income - Dividends Paid = Ending Retained Earnings

A company begins the year with $500,000 in retained earnings, generates $200,000 in net income during the year, and pays $50,000 in dividends to shareholders. The ending retained earnings would be calculated as:

$500,000 + $200,000 - $50,000 = $650,000

This formula reveals the direct relationship between profitability, distribution policies, and equity accumulation.

Companies that consistently generate positive net income while maintaining conservative dividend policies will see steady growth in retained earnings, while those with losses or aggressive dividend distributions may see retained earnings stagnate or decline.

The weighted consideration of these three components—beginning balance, current profitability, and distribution decisions—creates a dynamic that reflects both historical performance and current strategic choices.

Management teams can influence retained earnings growth through operational improvements that boost net income or dividend policy adjustments that alter the reinvestment rate.

This is where experienced financial leadership becomes invaluable in guiding the balance between rewarding shareholders today and building capabilities for tomorrow.

The retained earnings calculation might look simple, but the underlying decisions about profitability improvement and capital allocation require a sophisticated understanding of business cycles, growth opportunities, and stakeholder expectations that many growing companies struggle to navigate independently.

The statement of retained earnings serves as a bridge between the income statement and balance sheet, providing a detailed reconciliation of how current period profits or losses affected the company's accumulated equity.

While often presented as a separate financial statement, many companies incorporate this information within the statement of changes in shareholders' equity or as supplementary notes to the balance sheet.

For external stakeholders, the statement of retained earnings offers insights into management's capital allocation philosophy and dividend sustainability.

Investors can assess whether dividend payments are supported by current earnings or require dipping into accumulated profits, while lenders can evaluate the company's ability to build equity cushions that provide additional security for debt obligations.

In reality, the statement of retained earnings tells a story about management's confidence in future opportunities versus present shareholder returns.

Companies consistently retaining high percentages of earnings signal belief in internal growth prospects, while those paying out most profits as dividends suggest either limited reinvestment opportunities or a mature business model focused on shareholder income rather than growth.

Understanding the distinctions between these fundamental financial metrics prevents common confusion that can lead to misinterpretation of business performance and financial health:

Revenue represents the top line of business activity.

All money flowing into the company from sales, services, or other operating activities during a specific period makes up revenue.

This metric indicates market traction and business scale but doesn't reflect profitability or efficiency.

Net income shows the bottom-line result after deducting all expenses, taxes, and other costs from revenue. This figure reveals the company's ability to generate profit from operations and represents the periodic contribution to shareholder equity through earnings.

Retained earnings accumulate net income over time, minus any distributions to shareholders, creating a historical record of how much profit the company has reinvested in its operations.

This balance sheet item reflects long-term value creation rather than periodic performance.

So, as a company, you know now it's important to retain earnings for growth, but how are they actually deployed?

Retained earnings provide management with strategic flexibility to deploy accumulated profits across various value-creating initiatives without requiring external financing or shareholder approval for specific investments.

Common uses include:

The retained earnings balance and its trajectory over time provide valuable insights into company performance, management strategy, and financial health that extend far beyond simple profitability measures.

Companies with substantial retained earnings typically demonstrate consistent profitability, conservative dividend policies, and a long-term reinvestment focus.

These characteristics often indicate strong cash generation capabilities, disciplined capital allocation, and management confidence in internal growth opportunities.

High retained earnings can also signal mature companies with limited growth opportunities, leading to cash accumulation rather than value-creating reinvestment. In these situations, shareholders might prefer higher dividend distributions or share buyback programs that return excess capital.

Companies with minimal retained earnings may be in early development stages where profitability hasn't yet materialized, pursuing aggressive dividend policies that distribute most earnings to shareholders, or recovering from significant losses that depleted accumulated profits.

Often characterized by growth-stage companies that prioritize market expansion over near-term profitability, businesses facing industry disruption or operational challenges, or companies recovering from major write-offs, restructuring charges, or economic downturns.

In distressed situations, corporate debt restructuring may be necessary to restore financial stability.

The critical distinction most analysts miss: the direction and sustainability of retained earnings trends matter more than absolute levels.

A company with modest but consistently growing retained earnings often represents a better investment than one with high retained earnings that are stagnating or declining, as trends indicate future trajectory while balances reflect historical results.

Companies may optimize retained earnings differently based on their growth stage, competitive environment, and stakeholder expectations, making context crucial for accurate assessment. This is where financial planning and analysis expertise becomes invaluable.

It might be time to realize that your bookkeeper and controller can't be responsible for developing sophisticated retained earnings deployment strategies.

At this point, companies realize that as they grow, they need to bring on executive-level financial leadership that can transform accumulated profits into strategic competitive advantages.

Although there are certain training programs that can help bolster your financial team, such as CFO coaching and leadership development, in the meantime, it is a good idea to bring a fractional CFO on your team who can help optimize your capital allocation strategy as well as provide guidance to internal teams.

Understanding how to calculate and interpret retained earnings is just the beginning—implementing sophisticated financial planning that balances growth reinvestment with stakeholder returns requires experienced guidance. Whether you need fractional CFO support to establish robust financial reporting systems or interim leadership to guide strategic capital allocation decisions, experienced financial expertise can transform how your organization builds and deploys accumulated profits for long-term value creation.

Ready to optimize your retained earnings strategy?

Call McCracken Alliance today for a no-obligation consultation to turn your retained earnings into a competitive advantage.

Retained earnings are the total profits a company has earned over its lifetime, minus any dividends paid to shareholders. Think of it as the company's savings account that builds up from profitable operations and gets used to fund growth, pay down debt, or provide a financial cushion for tough times.

The retained earnings formula is: Beginning Retained Earnings + Net Income - Dividends Paid = Ending Retained Earnings. Each period, you add the current profit (or subtract losses) and subtract any dividends distributed to shareholders to get the new retained earnings balance.

No, retained earnings are not an asset. They appear in the shareholders' equity section of the balance sheet and represent the cumulative profits that have been reinvested in the business rather than distributed to owners. They're a source of financing, not a physical or financial asset.

Retained earnings increase with profitable operations and decrease with net losses or dividend payments. Other factors include stock dividends, prior period adjustments, treasury stock transactions, and certain accounting changes that can adjust the historical balance.

Yes, retained earnings can be negative, which creates an "accumulated deficit." This happens when a company's cumulative losses exceed its cumulative profits over time. It's common in early-stage companies or businesses recovering from significant challenges, and doesn't necessarily indicate current financial problems.

.svg)