Learn cash flow management strategies that connect liquidity to business performance. Includes forecasting steps, best practices & CFO-level

Learn cash flow management strategies that connect liquidity to business performance. Includes forecasting steps, best practices & CFO-level

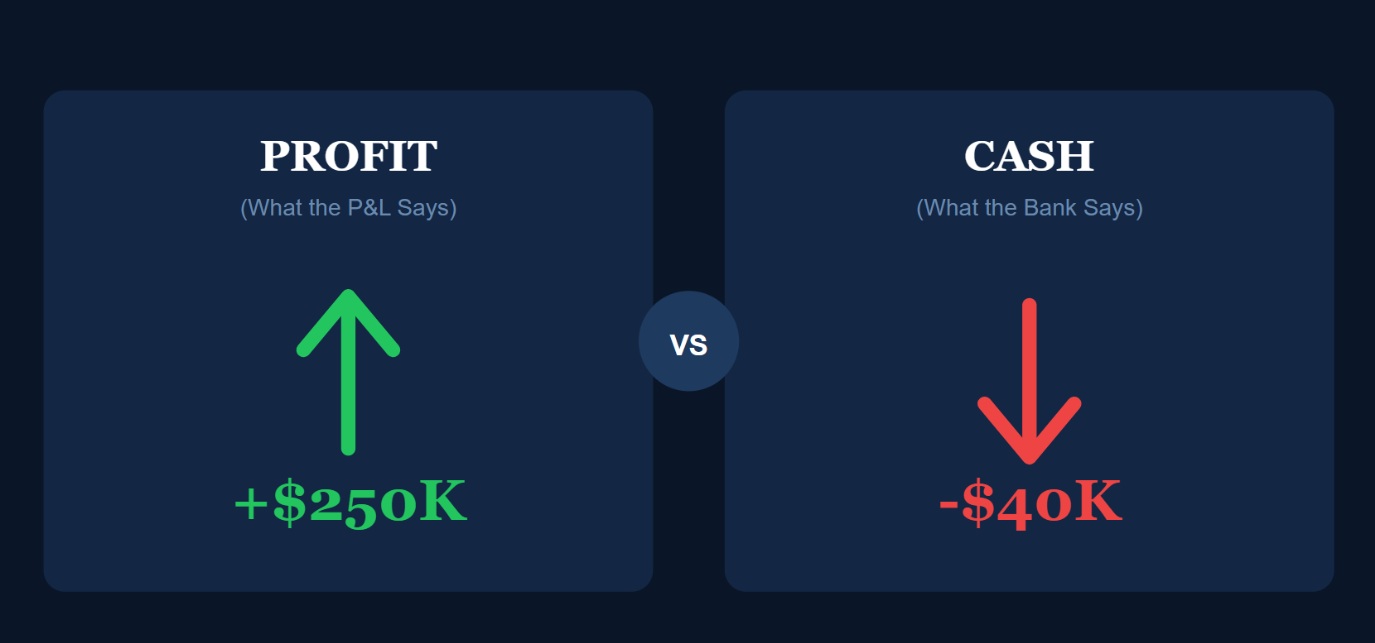

You closed your largest deal in the last quarter. The revenues are up. The P&L statement looks good.

So why are you scrambling to make payroll next Friday?

That is the cash flow paradox that catches a ton of businesspeople off guard.

“The bill is paid, and the revenue is booked,” but what the dollars in your bank account are telling you is a whole different story.

Your customers pay you in 60 days. Your employees want to get paid in 7. Your landlord doesn’t care about accrual accounting.

Profit is an idea. Money is survival.

And the difference between those two worlds is that businesses, even the successful ones, quietly strangle. Watching the inflows and outflows of cash, being ‘liquid’ in order to maintain the company’s working capital, isn’t just bookkeeping. It’s the difference that distinguishes scale from stagnation when the company’s statement looks great, but the checking account is empty.

This mini guide will lead you through cash flow management from understanding what it means to actually implementing it: What it means, why it’s so much more important to most CEOs and managers than it’s let on to be, and implementing it in order to distinguish well-managed businesses from those living check to check.

Cash flow management is all about observing, understanding, and adjusting where and when cash flows in and out of a business. It ensures that the business remains liquid enough to pay off its liabilities. Additionally, if there’s excess money, entrepreneurs could use it for business growth.

Here is the main distinction that trips up even seasoned business owners from time to time:

Profitability and cash flow arent the same exact thing.

A business can appear profitable despite the fact that its expenses exceeded its earnings. This occurs because accrual accounting allows a company to account for earnings when they occur, not when the money actually comes in. So a company can sell its product in March, but the money does not arrive until June. This means you have already incurred expenses to get the product completed.

That's where Cash flow management bridges the gap. It forces you to think in terms of

Not accounting abstractions

Cash flow management plugs the gap.

It forces you to think in terms of real money in the bank and when the money actually arrives, as opposed to accountant-speak.

Effective cash flow management means that you always know what your cash flow is and can pick up any cash flow problems before they become disasters and make decisions that will help your cash flow without stifling your business's expansion.

So if you’re wondering why your bank vault’s empty at the end of the month, read on to see how cash flow analysis can reveal the good, the bad, and the ugly about your business.

Each and every financial burden your company funds runs on CASH.

That's why they say ‘cash is king.’

With this, cash is key when it comes to:

Employees reasonably expect to be paid on time, regardless of the status of your largest client, who may be 45 days past due on their bill. Suppliers of goods or services extend credit to you because of your pattern of payments, and they will quickly stop extending credit to you if things appear uncertain.

Growth eats at cash like a wildfire through a forest. Hiring ahead of demand, stocking inventory for seasonal surges, R&D initiatives, and investing in equipment. And sure, from an entrepreneurial perspective, you would definitely require it to scale. However, these will cost money. Companies with unclear views regarding their finances would not be in a position to capitalize and could accrue debts they do not necessarily need, as they would not have the timeline to start reaping benefits.

Growth consumes money. Expanding staff before there’s a need, prepping for a peak in season, investing in gear before the money rolls in—all of those expansion strategies require actual money. Companies with unclear cash flow patterns sometimes overlook opportunities because of a lack of investment runway before the cash returns kick in.

Borrowers and investors focus on the health of cash flow as the key indicator of the viability of the business. When you manage cash flow effectively, you can look forward to favorable borrowing rates, sweet vendor offers, and the confidence of other investors who would like to see that you can manage the surprises that come along the way.

A company's total cash movement breaks down into three categories, each telling a different story about financial health and strategic direction. Understanding all three is essential—focusing on just one gives you an incomplete picture.

Operating cash flow represents the money generated (or consumed) by your core business activities. This includes all cash collected from customers (minus any cash paid for inventory, salaries,re,nt or other daily expenses used to keep your business running)

A positive cash flow means the business is generating enough to at least sustain operations.

A negative one, especially an extended means the core business model is going to require external funding just to keep the lights on.

Investing cash flow: This is money invested in long-term assets; in other words, it's stuff you invest in or sell, such as equipment or the purchase of another company or the divestiture of a division.

Just because there’s negative investing cash flow, it isn’t necessarily bad. It is often indicative that the company is making investments for future growth. It just depends on the situation. If you find that you’re spending lots of money on investments but not seeing the return, then the operating cash flow could be negatively affected.

Cash flow financing can be thought of as the money that flows between the business and the investors or the lenders. It may be the issuance of stocks, the payment of dividends, or the repurchasing of stocks.

It reveals where the company gets its money from. When a lot of what you are seeing is because of the funding of cash flow in order to fund operational deficits, this can be a concern. Utilizing funding in such a way as to fuel growth while maintaining good cash flow from operations is a whole different ball game altogether.

Cash flow forecasting transforms reactive scrambling into proactive planning. Here's a methodology that actually produces usable results:

Begin with what’s on the way in. Take a look at the receivables aging, the committed accounts, and the way you collect. Face facts—the invoice isn’t always collected. Your average collection period is 45 days. Don’t think that the customer is going to pay in 30.

Include all the money received from customers, loans, investment capital, sales proceeds, refunds, and all sources of money received by the business.

Next, ensure that you’re mapping every cash obligation on the horizon.

This includes fixed costs such as rent and salaries, as well as variable costs which differ based on expected activity levels. Don't forget the larger lump sum expenses such as quarterly tax payments, annual insurance premiums, and equipment maintenance.

Make sure you’re performing adequate forecasting and scenario planning that over, not underestimates costs.

This is when most projections go awry. You can see $100,000 in revenue coming in the following month, but when? Maybe it hits the 28th, but the payrolls go out on the 15th; you have an issue that the main screen won’t reveal.

When things are tight, create your forecast on a weekly or even daily basis. Time inflows and outflows to identify gaps before they arise.

Make sure forecasts are consistent. If you forecast in January and skip February, March’s numbers are obsolete. At best, forecast on a weekly rolling period and make sure actual results go into new projections. The best operators treat their cash flow projections as living documents, not static predictions.

Moving from understanding to action, here are the levers that actually improve cash position:

When your customers pay faster, your cash flow is healthier. A great idea is to offer your customers early payment discounts where it makes more sense. Also, technology, like an automated invoicing system, ensures that invoices are released immediately upon service delivery rather than being batched at month-end. Make payment easy—multiple options, clear instructions, minimal friction.

Track your cash conversion cycle to understand how long cash stays tied up in operations. Watch your quick ratio and current ratio for early warning signs. These metrics reveal trends that raw cash balances might hide.

Lengthening the period over which you pay the bill may be helpful for your cash flow management. Come up with a deal that suits you. Some sellers offer you a discount for early payment that is cheaper than your cost of capital.

Annual budgets get stale quickly. Use a 13-week cash forecast to stay connected to reality and to force yourself to check your cash position on a regular basis.

Knowing what not to do is half the battle. These patterns show up repeatedly in struggling businesses. So here's what NOT to do :

Even if your income statement says you're making money, your bank balance might be different. Operators who don't internalize this distinction consistently underestimate their cash needs and overestimate their financial flexibility.

DON’T ignore timing

Accrual accounting masks the delay between revenue recognition and cash collection. Think about that 90-day payment term with your biggest customer. That's a three-month operation fund without their contribution, even though your P & L shows the revenue coming in.

DON’T rely on one revenue stream.

We all have our heavy hitters when it comes to profitable customers. However, when 40% or more of your revenue comes from one client who suddenly slows payment, your entire cash position destabilizes. Diversification isn't just a revenue strategy—it's a cash flow survival strategy.

Having the right systems can make cash flow management way easier.

When you're really early stage, a spreadsheet might work. It could be a well-structured cash flow template that tracks weekly inflows, outflows, and running balances. Make sure you are always tracking your burn rate and updating weekly projections.

As complexity within your business grows, you might need something a bit ‘stronger.’

Platforms like High Radius, Data Rails, and the like can integrate with your existing accounting systems to automate data collection and provide real-time dashboards. Way less manual effort, way more efficiency.

However, in larger companies, the cash flow details will typically be directly entered into their ERP system or Treasury solution. The levels of sophistication will need to match the levels of complexity involved—who wants unnecessarily complex cash management in small businesses when this will simply end up costing more? But in complex businesses, there could be dangerous blind spots.

The fact of the matter is that most business owners know they should be in control of their cash flow. They understand the overarching idea. They’ve generated broad ‘forecasts’ or predictions.

But knowing ‘something’ in a broad sense, and having actionable, specific metrics, is quite another. And forecasting and determining cash flow rigorously and with the level of strategic guidance that translates cash flow management concepts from survival skills to a potent differentiator requires financial expertise.

There comes a time in every growing business where you just can’t exist on ‘vibes’ or ‘ideas’ of general cash flow alone anymore.

This is exactly where a Fractional CFO or Interim CFO creates disproportionate value.

They possess a level of forecasting rigor that enables accurate cash flow predictions. They establish tools and metrics that help share the information about your overall or company-wide cash position.

They identify changes and areas, such as payment terms and negotiations, that help improve your overall cash flow. Most importantly, they help relate overall cash flow management to other business strategic decisions.

They help forecast your business’s runway performance in relation to your hiring decision. They help forecast your business’s performance in terms of your expansion plans.

If you're spending more time worrying about cash than growing the business, it's probably time to bring in someone who can take that burden off your plate.

Don’t rush to the company vault to find out it's empty. Reach out to us today. Because cash flow shouldn't be a constant source of anxiety.

McCracken Alliance provides access to CFO-level professionals who understand both the mechanics of cash flow management and the strategic context that makes it meaningful.

Cash flow management ensures funds are set aside to repay bills and debts, but also directs money to make investments that make more money.

It is cash flow that determines whether a firm has the ability to pay its workers, its suppliers, make long-term investment decisions, or weather uncertainty. Profitable firms fail when cash flow goes dry.

First, calculate how much cash you really received. Next, list out every expense you encountered along the way. You have to factor in the difference between the expense recognition and the actual receipt of funds. Oh, and update the forecasts each week.

Profit = revenue - expenses as per accounting principles. Cash flow = this is the actual money flowing in and out of the bank account. You can have an accounting profit and still run out of money due to differences in when your revenue is booked versus when the money comes in.

.svg)